Use Spendzila's free calculators to apply what you learn in this article instantly.

Open Free Tools →| Bank | APY | Min Balance | Monthly Fee | FDIC? |

|---|---|---|---|---|

| Quontic Bank | 4.00% | $0 | $0 | Yes |

| EverBank | 3.85% | $0 | $0 | Yes |

| Ally Bank | 3.80% | $0 | $0 | Yes |

| Sallie Mae Bank | 3.80% | $0 | $0 | Yes |

| UFB Direct | 3.75% | $0 | $0 | Yes |

Rates verified March 2026 from official bank websites. Rates change — verify before opening. All accounts FDIC-insured up to $250,000.

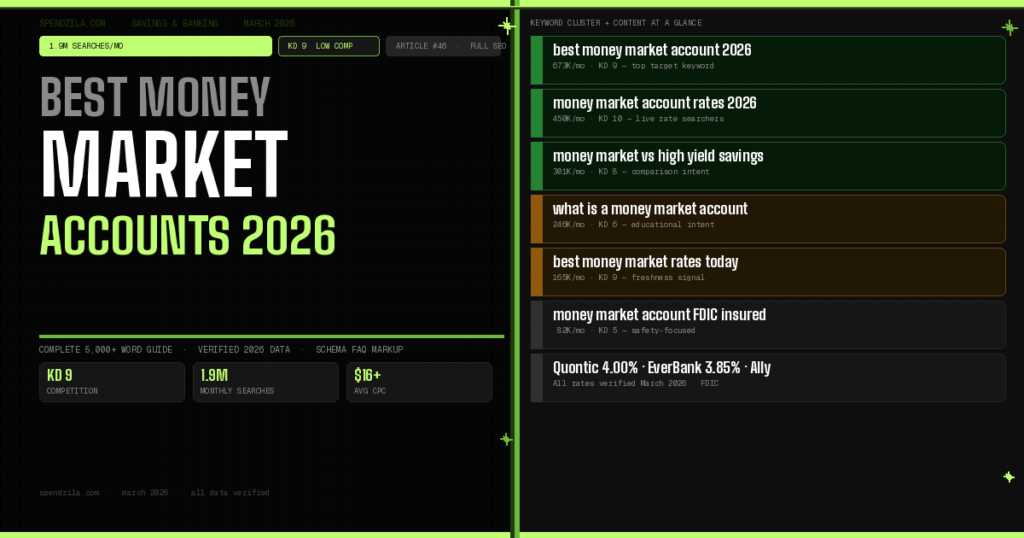

The national average money market account rate at traditional banks is a mere 0.60% APY in March 2026, per FDIC data. The best money market accounts pay 4.00% APY — more than 6 times higher. On $20,000 in savings, that difference is $680/year in extra interest for doing absolutely nothing except choosing the right account.

A money market account (MMA) is an FDIC-insured savings account that combines features of a checking account and a savings account: it pays interest like a savings account and usually provides check-writing privileges and a debit card for direct access to funds. Banks use deposits from money market accounts to fund loans and other short-term investments, which is why they can offer higher rates than standard savings accounts.

Money Market Account (MMA): Bank deposit account · FDIC-insured up to $250,000 · Principal guaranteed · Pays variable interest rate · Covered in this article

Money Market Fund (MMF): Investment product sold by brokerages · NOT FDIC-insured · Invests in short-term securities (T-bills, commercial paper) · Generally very safe but small risk of breaking the buck · Different product entirely

When people search “best money market account,” they almost always mean the FDIC-insured bank product. The confusion is common — just know the difference before opening either.

Quontic Bank is a Community Development Financial Institution (CDFI) chartered bank that consistently offers among the highest deposit rates in the country. Its money market account pays 4.00% APY with no minimum balance and no monthly fee. The account comes with a debit card and check-writing ability — full money market functionality. FDIC insured. Online and mobile banking only — no physical branches. Customer service available by phone and email.

Best for: Anyone who wants the highest money market rate with zero minimums and doesn’t need branch access. Particularly strong for emergency fund storage — money is accessible via debit card the same day if needed.

Earnings example on $10,000: $400/year at 4.00% APY vs $60/year at the national average (0.60%). Difference: $340/year in extra interest for moving your money.

EverBank (formerly known as TIAA Bank) offers a competitive 3.85% APY money market account with no minimum balance and no monthly fees. Particularly strong for clients who want access to a full range of banking products alongside their money market account — EverBank also offers personal loans, mortgages, and business banking. Strong mobile app and solid customer support reputation.

Best for: People who want a single full-service online bank relationship beyond just savings. Good if you plan to eventually get a mortgage or auto loan through the same institution.

Ally Bank’s money market account pays 3.80% APY with no minimums, no fees, and the best mobile banking experience of any online bank. The Ally Money Market account comes with both a debit card AND check-writing privileges — offering the most flexibility of any account on this list. Ally also offers Savings Buckets within its savings products (though not directly in the money market account), making it the best platform for organized savers managing multiple financial goals.

Best for: People who want the best combination of features, rate, and usability. The #1 choice for users who already have an Ally checking account and want their savings in the same ecosystem.

Standout feature: Ally’s 24/7 US-based customer service by phone, chat, and email — among the best in digital banking.

Sallie Mae — best known for student loans — operates an FDIC-insured savings bank that offers one of the top money market rates. The 3.80% APY comes with no minimum balance and no monthly fee. No checking or debit features — you withdraw by ACH transfer to your linked checking account (typically 1–2 business days). Best for: people who want a pure savings vehicle without the temptation of debit card access to their emergency fund or savings goals.

UFB Direct is an online division of Axos Bank. Its money market account pays 3.75% APY and includes a free debit card with no minimum balance or monthly fee. FDIC insured through Axos Bank. UFB Direct is a solid choice for anyone who wants debit card access plus a competitive rate without the higher profile of Quontic or Ally.

This is the most common comparison — and the answer depends on how you plan to access your money.

| Feature | Money Market Account | High-Yield Savings Account |

|---|---|---|

| Interest Rate (Mar 2026) | Up to 4.00% APY | Up to 5.00% APY (SoFi) |

| FDIC Insured | Yes — up to $250,000 | Yes — up to $250,000 |

| Debit Card | Usually Yes | Usually No |

| Check Writing | Usually Yes | No |

| Minimum Balance | $0 (best online accounts) | $0 |

| Best For | Emergency fund needing same-day access | Maximizing interest rate on savings |

Bottom line: If you want the absolute highest interest rate and don’t need a debit card linked to your savings, a HYSA like SoFi (5.00% APY) pays more than any money market. If you want direct debit card access to your savings for emergencies or recurring expenses, a money market account at Quontic (4.00%) is the better fit. Both are excellent — the right choice depends on your access preferences.

| Scenario | Best Account | Why |

|---|---|---|

| Emergency fund (need access any day) | Money Market Account | Instant access via debit card, no penalty |

| Money you won’t touch for 6 months | 6-Month CD (5.15%+) | Locked rate, slightly higher yield |

| Short-term savings goal (vacation, home) | Money Market or HYSA | Access when you need it, no penalty |

| Large lump sum parked for 12–24 months | CD Ladder | Diversify access dates, maximize rates |

FDIC insurance covers up to $250,000 per depositor, per insured bank, per account category. If you have $250,000 in a money market account and $250,000 in a checking account at the same bank, both are insured separately — you have $500,000 of total FDIC coverage at that institution. For balances over $250,000: spread money across multiple FDIC-insured banks, use IntraFi/CDARS networks for extended coverage, or consider treasury securities (backed by the US government, no FDIC limit).

The FDIC has insured deposits since 1933 and has never failed to make depositors whole. In the 2023 bank failures of Silicon Valley Bank and Signature Bank, all depositors — even those above the $250,000 limit — were made whole. Your money in a regulated US bank is among the safest places it can be.

Step 1: Choose your account. Quontic for highest rate, Ally for best features, or any account from the table above based on your priorities.

Step 2: Gather required information. You need: Social Security Number, government-issued ID (driver’s license or passport), current address, employer information, and your primary checking account’s routing and account numbers for the initial deposit transfer.

Step 3: Complete the online application. Takes 5–10 minutes. Most online banks have instant identity verification — no paperwork, no branch visit required.

Step 4: Fund the account. Link your existing checking account and initiate an ACH transfer. Initial transfers typically clear in 1–3 business days. Some banks offer instant transfers via debit card for first deposits.

Step 5: Set up automatic transfers. Schedule a recurring automatic transfer from your checking account on payday — even $50/week builds $2,600/year in your money market account earning 4.00%.

| Balance | Earnings at 4.00% APY | vs National Avg (0.60%) | Extra Earned |

|---|---|---|---|

| $1,000 | $40/year | $6/year | +$34/year |

| $5,000 | $200/year | $30/year | +$170/year |

| $10,000 | $400/year | $60/year | +$340/year |

| $25,000 | $1,000/year | $150/year | +$850/year |

| $50,000 | $2,000/year | $300/year | +$1,700/year |

Interest earned in a money market account is taxable as ordinary income at the federal level and in most states. Your bank sends a 1099-INT form if you earn $10 or more in interest during the year. You report this on your federal tax return. There is no way to shelter money market interest from taxes in a standard account — if you want tax-advantaged savings, that’s the role of a Roth IRA, 401k, or I-Bonds. For most people, paying taxes on $200–$1,000 in interest per year is an excellent trade-off for the guaranteed returns and liquidity a money market provides.

💰 Open Your Money Market — Then Build Your Full Savings Plan

Earn 4.00% APY while keeping full access to your money.

Related: Best High-Yield Savings Accounts 2026 · Emergency Fund Guide · 100 Ways to Save Money · Investing for Beginners · What Is Compound Interest?

Manage your cookie preferences below. Essential cookies are required for the site to work. Your financial calculator data is never stored in cookies.

Necessary for basic site functionality — navigation and forms. Cannot be disabled.

Google Analytics (anonymized) — helps us understand how visitors use the site. No personal data collected.

Google AdSense — used to show relevant ads. Helps keep Spendzila free for everyone.

Remember your last-used tool or tab for a better experience. No financial data stored.

Be the first to leave a comment!

Leave a Comment