Use Spendzila's free calculators to apply what you learn in this article instantly.

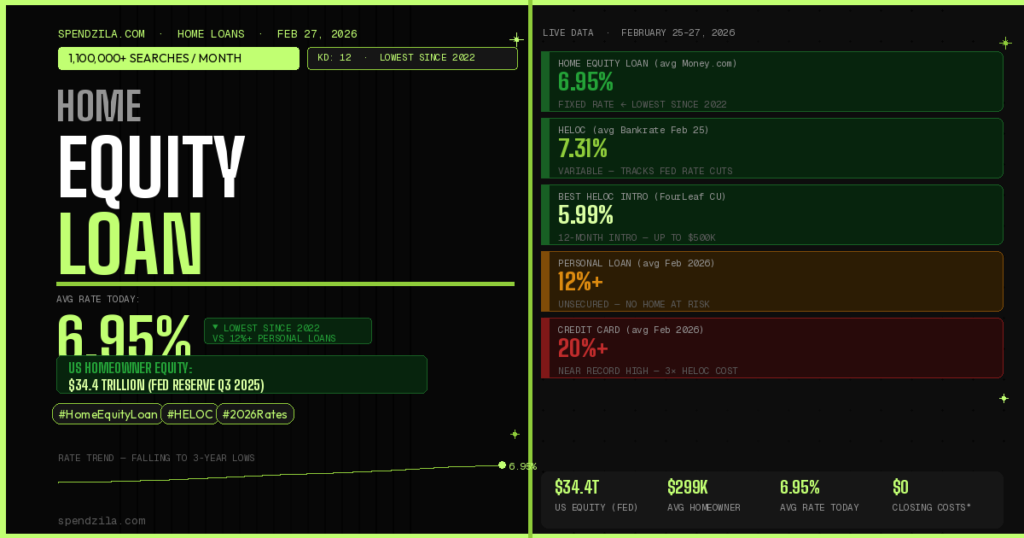

Open Free Tools →American homeowners are sitting on more wealth than at any other point in history — and right now, borrowing against it has never been more affordable. US homeowners collectively hold $34.4 trillion in equity as of Q3 2025 (Federal Reserve), and home equity loan rates just dropped to their lowest level since 2022, with the average now sitting at 6.95% according to Money.com’s February 20, 2026 survey.

If you own a home and need to borrow money — for renovations, debt consolidation, education, or any other major expense — a home equity loan gives you access to large sums at rates that are a fraction of what credit cards (20%+) and personal loans (12%+) currently charge. This complete guide covers exactly how home equity loans work, today’s live rates, what you need to qualify, the best lenders, and step-by-step instructions to get the best deal in 2026.

📉 Avg home equity loan rate (Money.com): 6.95% — lowest since 2022

📉 Avg HELOC rate (Bankrate): 7.31% — near 3-year low

💰 Total US homeowner equity: $34.4 trillion (Fed Reserve, Q3 2025 — record high)

🏆 Best available HELOC intro rate: 5.99% (FourLeaf Credit Union, 12 months)

🔮 Forecast: 3 more Fed cuts in 2026 → HELOC rates expected to fall another 0.75%

A home equity loan — sometimes called a second mortgage or a home equity installment loan — lets you borrow a lump sum of cash using your home’s equity as collateral. Equity is the portion of your home you actually own: your home’s current market value minus whatever you still owe on your mortgage.

For example: if your home is worth $400,000 and you owe $250,000 on your mortgage, you have $150,000 in equity. Most lenders let you borrow up to 80–85% of your home’s total value (including your first mortgage), which means you could potentially access $70,000–$90,000 through a home equity loan.

| Feature | Details (2026) |

|---|---|

| Loan type | Secured installment loan (lump sum) |

| Interest rate type | Fixed — locked for the entire loan term |

| Average rate (Feb 27, 2026) | 6.95%–8.07% depending on source and term |

| Typical loan amounts | $10,000 – $500,000+ |

| Repayment terms | 5 – 30 years |

| Minimum equity required | 15–20% equity in the home (most lenders) |

| Minimum credit score | 620 (most lenders); 680+ for best rates |

| Average homeowner equity available | $299,000 (Cotality Q3 2025); $212,000 tappable (ICE June 2025) |

| Risk | Your home is collateral — foreclosure possible if you default |

Rates vary significantly across sources, lenders, and loan terms. Here’s the complete picture from all major data sources as of February 25–27, 2026:

| Product / Term | Rate | Source | As Of |

|---|---|---|---|

| Home Equity Loan (avg, Money.com) | 6.95% ← Lowest since 2022 | Money.com survey | Feb 20, 2026 |

| Home Equity Loan (5-yr, Bankrate) | 7.87% | Bankrate national avg | Feb 25, 2026 |

| Home Equity Loan (10-yr, Bankrate) | 8.07% | Bankrate national avg | Feb 25, 2026 |

| Home Equity Loan (15-yr, Bankrate) | 8.06% | Bankrate national avg | Feb 25, 2026 |

| Home Equity Loan (avg, Curinos) | 7.44–7.59% | Curinos analytics | Feb 2026 |

| HELOC avg (Bankrate) | 7.31% | Bankrate national avg | Feb 25, 2026 |

| HELOC avg (Curinos) | 7.23–7.25% | Curinos analytics | Feb 2026 |

| Best HELOC intro rate (FourLeaf CU) | 5.99% (12 months, up to $500K) | FourLeaf Credit Union | Feb 2026 |

| Strong credit borrowers can reach | 6.50%–7.50% | The Mortgage Reports / Bankrate expert | Feb 24–25, 2026 |

The Federal Reserve cut its benchmark rate three times in 2025 (September, October, and December) by 0.25% each time, bringing the Fed funds rate to 3.5%–3.75%. Since HELOC rates are tied directly to the prime rate (currently 6.75%), each cut flows through to borrowers almost immediately. Home equity loan rates, tied more to longer-term Treasury yields, have also drifted down as markets price in further cuts. Experts quoted by Bankrate forecast three more quarter-point Fed cuts in 2026 — which would push HELOC rates down by another 0.75% and further lower home equity loan rates.

This is the most important decision for home equity borrowers. Both use your home as collateral and offer rates far below credit cards — but they work very differently:

| Feature | Home Equity Loan (HEL) | HELOC |

|---|---|---|

| How funds work | Lump sum at closing | Revolving credit line — draw as needed |

| Interest rate | Fixed — never changes | Variable — changes with prime rate |

| Current avg rate (Feb 2026) | 6.95%–8.07% | 7.23%–7.31% |

| Monthly payment | Fixed and predictable from day one | Variable — changes as rate and balance change |

| Draw period | None — full amount disbursed upfront | Typically 10 years (interest-only payments) |

| Repayment period | 5–30 years (starts immediately) | 20 years after draw period ends |

| Closing costs | 2–5% of loan amount | Low or none at many lenders |

| Best for | One large one-time expense with predictable repayment | Ongoing or multiple expenses over time |

| Rate risk | None — locked at closing | High if rates rise; benefit if rates fall further |

| Your Situation | Best Choice | Reason |

|---|---|---|

| Single large project (kitchen remodel, medical bill) | Home Equity Loan | Fixed rate, predictable payment, lump sum |

| Ongoing or phased projects (multi-phase renovation) | HELOC | Draw only what you need; pay interest only on drawn amount |

| You hate payment uncertainty / on a fixed income | Home Equity Loan | Fixed rate never changes; budget-friendly |

| You expect rates to fall further in 2026 | HELOC | Variable rate drops automatically with Fed cuts |

| Debt consolidation — paying off credit cards | Home Equity Loan | Fixed lower rate replaces variable 20%+ card rates permanently |

Most lenders cap your total borrowing at 80–85% of your home’s appraised value, across all loans combined (first mortgage + home equity loan). This is called the combined loan-to-value (CLTV) ratio.

Maximum Borrowable Amount = (Home Value × 0.85) − Current Mortgage Balance

| Home Value | Mortgage Owed | Your Equity | Max Borrow (80% CLTV) | Max Borrow (85% CLTV) |

|---|---|---|---|---|

| $300,000 | $200,000 | $100,000 | $40,000 | $55,000 |

| $400,000 | $250,000 | $150,000 | $70,000 | $90,000 |

| $500,000 | $300,000 | $200,000 | $100,000 | $125,000 |

| $600,000 | $350,000 | $250,000 | $130,000 | $160,000 |

| $750,000 | $400,000 | $350,000 | $200,000 | $237,500 |

Your credit score dramatically affects what rate you’ll receive. Here’s what different credit tiers can expect in February 2026:

| FICO Score | Credit Tier | Typical HEL Rate | Monthly Payment* | Total Interest* |

|---|---|---|---|---|

| 760–850 | Exceptional | 6.50%–7.00% | $565–$582/mo | $17,900–$19,920 |

| 720–759 | Very Good | 7.00%–7.75% | $582–$604/mo | $19,920–$22,440 |

| 680–719 | Good | 7.75%–8.50% | $604–$622/mo | $22,440–$24,640 |

| 640–679 | Fair | 8.50%–10.00% | $622–$660/mo | $24,640–$29,200 |

| 580–639 | Poor | 10.00%–13.00%+ | $660–$752+/mo | $29,200–$40,240+ |

*Based on $50,000 home equity loan, 10-year term. February 2026 rate estimates. For illustration only.

Here’s exactly what you’d pay monthly and in total interest at today’s average rate of 7.87% (Bankrate 5-year) across common loan amounts and terms:

| Loan Amount | 5-yr @ 7.87% | 10-yr @ 8.07% | 15-yr @ 8.06% | vs Credit Card @ 20%* |

|---|---|---|---|---|

| $25,000 | $507/mo · $5,420 int | $305/mo · $11,600 int | $241/mo · $18,380 int | $667/mo · $55,020 int |

| $50,000 | $1,014/mo · $10,840 int | $609/mo · $23,080 int | $482/mo · $36,760 int | Minimum pmts only: 40+ yrs |

| $75,000 | $1,521/mo · $16,260 int | $914/mo · $34,680 int | $723/mo · $55,140 int | Interest alone: $1,250/mo |

| $100,000 | $2,028/mo · $21,680 int | $1,218/mo · $46,160 int | $964/mo · $73,520 int | Interest alone: $1,667/mo |

*Credit card at 20% APR paying minimum 2% of balance monthly. Home equity loan payments are estimates. For illustration only.

| Requirement | Minimum | Ideal for Best Rate |

|---|---|---|

| Home equity | 15–20% equity in the property | 30–40%+ equity (lower CLTV = better rate) |

| Credit score | 620 (some lenders allow below 600) | 720+ for competitive rates; 760+ for best |

| Debt-to-income (DTI) | Below 43–50% (lender dependent) | Below 36% |

| Income / employment | Verifiable income (W-2, tax returns, bank statements) | 2+ years stable employment history |

| Combined LTV ratio | Below 85–90% CLTV (some lenders) | Below 70% CLTV (Curinos/best-rate baseline) |

| Property type | Primary residence preferred; second homes possible | Primary single-family home = best rates |

| Use Case | Why It Makes Sense | Tax Deductible? |

|---|---|---|

| Home improvements / renovations | Adds value to the collateral itself; deductible interest | Yes |

| High-interest debt consolidation | Replace 20%+ credit card rate with 7–8% fixed rate; saves thousands | No (not home-related) |

| Major medical expenses | Far cheaper than medical financing or credit cards | No |

| Down payment on investment property | Leverage equity to acquire income-generating assets | Possibly (consult tax advisor) |

This is one of the most frequently misunderstood aspects of home equity loans. Here’s the accurate 2026 answer:

Yes — but only for home-related expenses. The IRS allows you to deduct home equity loan interest only if the loan proceeds were used to “buy, build, or substantially improve” the home that secures the loan. This means:

| Detail | 2026 Rules |

|---|---|

| Eligible use | Buy, build, or substantially improve the secured home only |

| Total deduction cap | Combined mortgage + HEL debt of up to $750,000 ($375,000 if married filing separately) |

| Requires itemizing | Yes — you must itemize deductions (Schedule A), not take the standard deduction |

| SALT cap change (OBBBA 2026) | SALT cap raised to $40,000 for married couples in 2026 — makes itemizing more attractive for more homeowners |

| Lender | Rate Range | Loan Amounts | Min. Credit | Best For |

|---|---|---|---|---|

| FourLeaf Credit Union | 5.99% intro HELOC (12 mo) | Up to $500,000 | 780+ | 🏆 Best HELOC intro rate |

| Spring EQ | Competitive — fast funding | $25K–$500K | 640 | 🏆 Fastest funding (5 days) |

| Figure | Competitive HELOC | $15K–$400K | 640 | 100% online; 5-day closing |

| Third Federal S&L | Very competitive; rate match guarantee | $10K–$200K | 680 | 🏆 Rate match guarantee |

| Discover Home Loans | Competitive; $0 closing costs | $35K–$300K | 620 | 🏆 $0 closing costs |

| PenFed Credit Union | Among lowest for HEL | $25K–$500K | Not published | Best rates for credit union members |

| Your Local Credit Union | Often 0.25–0.75% below banks | Varies | Varies | Best for existing members; rate advantage over banks |

Before applying, get your free credit score from Credit Karma or AnnualCreditReport.com, and estimate your home’s current value at Zillow or Redfin. Calculate your approximate equity using the formula above. This tells you exactly which tier you’re in and what rates to expect. If your credit is below 680, spending 60–90 days improving it first could save thousands in interest. See: What Is a Good Credit Score?

Lenders may approve you for more than you need. Borrow only what you need for your specific purpose — every extra dollar increases your monthly payment and total interest. If you’re consolidating $40,000 in debt, borrow $40,000. Resist the temptation to take extra “just in case.”

Rate differences of 0.5–1.5% between lenders on the same home equity loan are common. On a $75,000 loan over 10 years, a 1% rate difference is over $4,000 in total interest. Get quotes from your current mortgage lender, your bank/credit union, and 2–3 online lenders like Discover or Figure. Pre-qualification uses soft inquiries — your credit score is unaffected until you formally apply.

Once you’ve chosen the best offer, submit a full application with all required documents. The lender will order an appraisal ($300–$700) to verify your home’s value — this is normal and required. Most home equity loans close in 2–6 weeks. Some newer online lenders (Figure, Spring EQ) can close in as little as 5 business days.

Before closing, you’ll receive a Closing Disclosure showing all final loan terms, rate, fees, and payment schedule. Check every number: the interest rate must match what was quoted, closing costs should match the Loan Estimate, and there should be no surprise fees. You have a 3-day right of rescission after closing — you can cancel within 3 business days of signing without penalty.

| Feature | Home Equity Loan | Cash-Out Refinance | Personal Loan | Credit Card |

|---|---|---|---|---|

| Avg rate (Feb 2026) | 6.95–8.07% | 6.50% (new 1st mtg) | 12%+ | 20%+ |

| Affects 1st mortgage? | No — keeps your low rate | Yes — replaces it entirely | No | No |

| Closing costs | 2–5% of loan amount | 2–5% of full loan | 0–8% origination | None |

| Home as collateral? | Yes | Yes | No | No |

| Best for (2026) | Large expense; keep existing low mortgage rate | Your current mortgage rate is higher than 6.5%; need large sum | No home equity; smaller amounts; fast funding | Small short-term purchases paid off monthly |

Moving from 680 to 720 can cut 0.5–1% off your home equity loan rate. On a $75,000 loan over 10 years, that’s $4,000+ in savings. Pay down credit card balances below 30% utilization, dispute any credit report errors, and avoid new credit applications for 90 days before applying. See: What Is a Good Credit Score?

Borrowing less relative to your home’s value earns a lower rate. If you can borrow $60,000 instead of $80,000 against a $400,000 home, your CLTV drops from 70% to 65% — pushing you into a better pricing tier with most lenders. Borrow only what you genuinely need.

Credit unions routinely offer home equity loan rates 0.25–0.75% lower than major banks — they’re nonprofit and pass savings to members. If you’re not a credit union member, joining is often free or low-cost. Add your current mortgage lender (who already has your file) and 2–3 online lenders to the comparison. Multiple inquiries within 30–45 days are counted as one by FICO.

A 5-year home equity loan carries a lower rate than a 15-year term at most lenders. If cash flow allows, choosing the shorter term both reduces your rate and dramatically reduces total interest paid — though it increases monthly payments.

Most lenders offer 0.25–0.50% rate reductions for setting up automatic payments. This is free money — always enroll in autopay when offered. On a $75,000 loan, 0.25% off is approximately $1,800 saved over 10 years.

Several lenders (notably Discover) offer home equity loans with $0 closing costs. Others waive costs for existing customers or those enrolling in autopay. Before comparing rates, always ask each lender to quote the APR including all fees — some lenders quote a lower rate but charge higher closing costs that offset the savings.

Three more Fed rate cuts are forecast for 2026. If they materialize, HELOC rates would drop from ~7.31% to ~6.56%. If you have flexibility in your project timeline and cash flow stability to handle variable payments, a HELOC could end up costing less than locking in today’s fixed home equity loan rate — especially for borrowers who can repay within 2–3 years.

Lenders tell you how much you’re approved for — not how much you should borrow. Many homeowners see a $150,000 approval and borrow $120,000 when they only needed $60,000. Every extra dollar you borrow costs interest for years. Borrow for a specific purpose with a specific amount, then stop.

The first lender you try — often your existing mortgage lender or bank — is rarely the best. Rate differences of 0.5–1.5% on home equity loans between lenders are common. On $75,000 over 10 years, that’s $4,000–$12,000 in unnecessary interest. Always compare at least 3–5 lenders.

Using your home’s equity to finance a vacation, luxury car, or consumer electronics puts your home at risk for spending that produces zero long-term value. If a market downturn reduces your home’s value simultaneously, you could face negative equity while still owing on the loan.

A lender quoting 7.50% with $3,000 in closing costs may actually cost more than one quoting 7.75% with zero closing costs, depending on how long you hold the loan. Always compare APR (which factors in fees) and ask each lender for a Loan Estimate to compare total costs on equal terms.

Unlike a personal loan or credit card default — which damages your credit — a home equity loan default can end with you losing your home. Before taking any home equity loan, ensure you have a stable income, a realistic repayment plan, and a clear understanding that your home is on the line. Never borrow home equity as a last resort to cover ongoing living expenses; address the underlying financial issue instead. See our debt consolidation guide and saving money guide.

As of February 27, 2026, home equity loan rates range from 6.95% (Money.com average) to 8.07% (Bankrate national average for 10-year terms), depending on the data source, loan term, lender type, and your credit profile. Curinos analytics data shows an average of 7.44–7.59%. Strong credit borrowers can access rates in the low-to-mid 6% range by shopping credit unions and comparing multiple lenders. These are near the lowest levels since 2022, reflecting the Fed’s three rate cuts in 2025 and expectations of further cuts in 2026.

A home equity loan provides a lump sum at a fixed interest rate, with equal monthly payments over a set term (typically 5–30 years). A HELOC is a revolving credit line with a variable interest rate — you can draw funds as needed during the draw period (usually 10 years), pay interest only on what you borrow, and repay the full balance during the repayment period. Home equity loans offer payment certainty; HELOCs offer flexibility and the potential benefit of falling rates. In 2026 with three Fed cuts forecast, HELOCs have an additional appeal — variable rates should decline further as the year progresses.

Most lenders allow you to borrow up to 80–85% of your home’s appraised value, minus what you still owe on your mortgage. The formula is: (Home Value × 0.80–0.85) − Mortgage Balance = Maximum Home Equity Loan. Example: $400,000 home × 80% = $320,000 − $250,000 mortgage = $70,000 maximum loan. The average US homeowner has approximately $299,000 in total equity (Cotality Q3 2025) and $212,000 in tappable equity (ICE June 2025 data).

For homeowners with genuine need, sufficient equity, and stable income to make payments, now is one of the best times to borrow against home equity in 3+ years. Rates have declined significantly from 2023–2024 highs and are at multi-year lows. Meanwhile, US homeowners collectively hold a record $34.4 trillion in equity. The key caveats: your home is collateral (default risk is foreclosure, not just credit damage), and you should never borrow home equity for speculative investments or depreciating expenses. For debt consolidation, home improvements, or large one-time expenses, a home equity loan at 7–8% is far cheaper than personal loans (12%+) or credit cards (20%+).

Most lenders require a minimum credit score of 620 for a home equity loan. However, the best rates — in the low-to-mid 6% range — typically require 720+ credit, and some of the most competitive lenders (like those used for Curinos benchmarks) require 780+ for their best published rates. If your score is below 680, spending 2–3 months improving it before applying can meaningfully reduce your rate and total interest paid. See: What Is a Good Credit Score?

Yes, and for many homeowners this is the best financial move available. Consolidating $50,000 of credit card debt at 20% APR into a home equity loan at 8% over 10 years saves over $32,000 in interest and dramatically reduces your monthly payment burden. The key risk: you’re converting unsecured credit card debt into debt secured by your home. If you default, your home could be foreclosed rather than just your credit damaged. This math strongly favors consolidation for disciplined borrowers who won’t re-run the credit card balances after consolidation. See our full Debt Consolidation Guide.

Traditional banks and lenders take 2–6 weeks from application to funding — the appraisal, underwriting, and title search all take time. Online-focused lenders like Figure and Spring EQ have streamlined the process and can close in as little as 5 business days using automated appraisals and digital document processing. If speed matters for your use case, prioritize lenders advertising fast funding timelines.

If you miss payments on a home equity loan, the lender will initially charge late fees and report missed payments to credit bureaus (which damages your credit score). After 90–120 days of non-payment, the lender can begin foreclosure proceedings — a legal process to seize and sell your home to recover the debt. Because home equity loans are secured by your property, defaulting carries far more serious consequences than defaulting on a personal loan or credit card. If you anticipate difficulty making payments, contact your lender immediately — many have hardship programs, modification options, or temporary forbearance that are far better than allowing the loan to go into default.

Home equity loan rates are near their lowest level since 2022 — and US homeowners are sitting on a record $34.4 trillion in equity. The average homeowner has $299,000 in equity and $212,000 in tappable funds. For any homeowner who needs to borrow a significant amount of money for the right reasons, 2026 represents one of the best opportunities in recent years to access cheap, secured capital.

Your action plan:

If you’re using a home equity loan for debt consolidation, read our complete Debt Consolidation Guide. If you need to build savings before applying, see: How to Save Money Fast. And use the 50/30/20 budget rule to ensure your new home equity loan payment fits your overall financial picture.

💳 Build the Credit Score That Unlocks the Best Rates

A 760+ credit score can get you home equity loan rates in the low-to-mid 6% range — potentially saving $5,000–$15,000+ in interest on a $75,000 loan. A $0 annual fee cash back card used responsibly builds credit faster while earning rewards on every purchase.

Be the first to leave a comment!

Leave a Comment