Use Spendzila's free calculators to apply what you learn in this article instantly.

Open Free Tools →Applying for your first credit card is a big milestone — and it’s easier than most people think. The entire process takes less than 10 minutes online, and many applicants receive an instant decision.

But knowing how to apply the right way can mean the difference between approval and rejection. In this guide, we walk you through every step — from checking your eligibility to submitting your application and activating your new card.

Before jumping into the application, it’s worth taking a moment to check whether you meet the basic requirements. In the United States, credit card issuers follow federal rules that determine who qualifies.

Basic eligibility requirements:

Getting your information ready ahead of time makes the application process smooth and fast. Here’s exactly what you’ll need:

One of the biggest mistakes first-time applicants make is applying for the wrong card. Each application creates a hard inquiry on your credit report, which can temporarily lower your score. So choose wisely before you apply.

If you are currently enrolled in college or university, apply for a student credit card. These have the easiest approval requirements and often offer rewards on categories students use most — like dining, streaming services, and Amazon.

Look for cards that explicitly state “no credit history required.” The Capital One Platinum and Petal 2 Visa are excellent options. The Petal card is unique because it evaluates your bank account history instead of your credit score.

Cards like the Capital One QuicksilverOne are designed for this range. They may have a small annual fee but offer cash back rewards in return.

| Feature | Secured Card | Unsecured Card |

|---|---|---|

| Deposit Required | Yes ($200–$500 typically) | No |

| Approval Ease | Very easy | Moderate |

| Builds Credit | Yes | Yes |

| Rewards | Rare | Common |

| Best For | Rebuilding or starting credit | First-time applicants with income |

Here is the complete process from start to finish:

If you’ve ever had a loan, been added as an authorized user on someone’s card, or opened a bank account, you may already have a credit score. Check it for free at AnnualCreditReport.com or through your bank’s app. This tells you which cards you’re most likely to qualify for.

Most major issuers — Capital One, Discover, Chase — offer a pre-qualification tool on their websites. This uses a soft inquiry (which does NOT affect your credit score) to show you which cards you’re likely to be approved for. Always use this before formally applying.

Always apply directly through the issuer’s official website (e.g., capitalone.com, discover.com, chase.com). Avoid third-party sites that may not offer the most current terms or could be fraudulent.

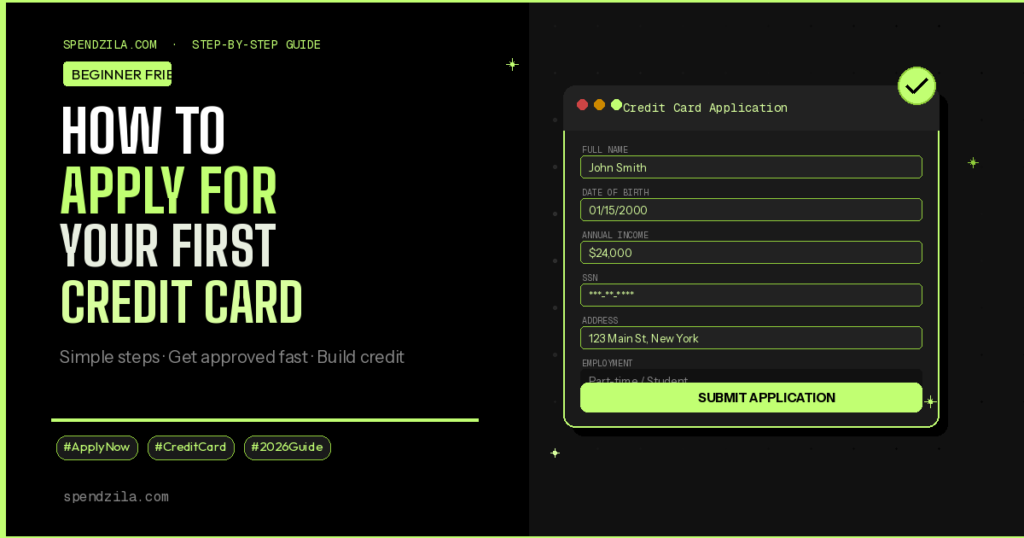

The online form typically asks for:

Double-check all information before submitting. Errors can cause delays or automatic rejections.

After hitting submit, most issuers provide one of three responses:

Once your physical card arrives (usually within 7–10 business days), activate it through the issuer’s website or by calling the number on the back of the card. Your card is not usable until it’s activated.

Create your online account immediately and set up autopay for at least the minimum payment. This ensures you never miss a payment, which is the single most important factor in building good credit.

Here’s what to expect once your application is submitted:

| Timeline | What Happens |

|---|---|

| Immediately | Hard inquiry posted to your credit report (–5 to –10 points temporarily) |

| Within minutes | Instant approval or denial decision (most of the time) |

| 7–14 days | Physical card arrives in the mail if approved |

| 30 days | New account appears on your credit report |

| 3–6 months | Credit score starts improving with responsible use |

Getting rejected is disappointing but not the end of the road. Here’s what to do:

The online application itself takes 5–10 minutes. Most applicants receive an instant decision. If approved, the physical card arrives within 7–10 business days.

Yes, a hard inquiry temporarily lowers your score by 5–10 points. This effect typically disappears within 3–6 months. The long-term benefit of building credit far outweighs this short-term dip.

Yes. You can list other forms of income such as freelance work, part-time income, allowances, scholarships, financial aid, or investment income. You must be able to show some ability to make payments.

You must be at least 18 years old. If you are between 18 and 20, you must show proof of independent income or have a co-signer who is 21 or older.

Yes, if you have an ITIN (Individual Taxpayer Identification Number). Some issuers like Deserve EDU even allow international students to apply without an SSN using their passport and visa information.

Use the pre-qualification tools on Capital One, Discover, and Chase websites. These use soft inquiries and show you likely approvals without affecting your credit score.

Applying for your first credit card is a simple, fast process — but doing it the right way makes a big difference. Choose a card that matches your credit profile, use the pre-qualification tool first, and have all your information ready before you start the application.

If you haven’t already, check out our guide on the Best First Credit Cards for Beginners in 2026 to find the perfect card before you apply. Once you’re approved, use it responsibly, pay it off every month, and you’ll be on your way to an excellent credit score faster than you think.

Ready to Apply for Your First Credit Card?

Read our complete guide to the best beginner credit cards of 2026 before you apply.

Be the first to leave a comment!

Leave a Comment