Use Spendzila's free calculators to apply what you learn in this article instantly.

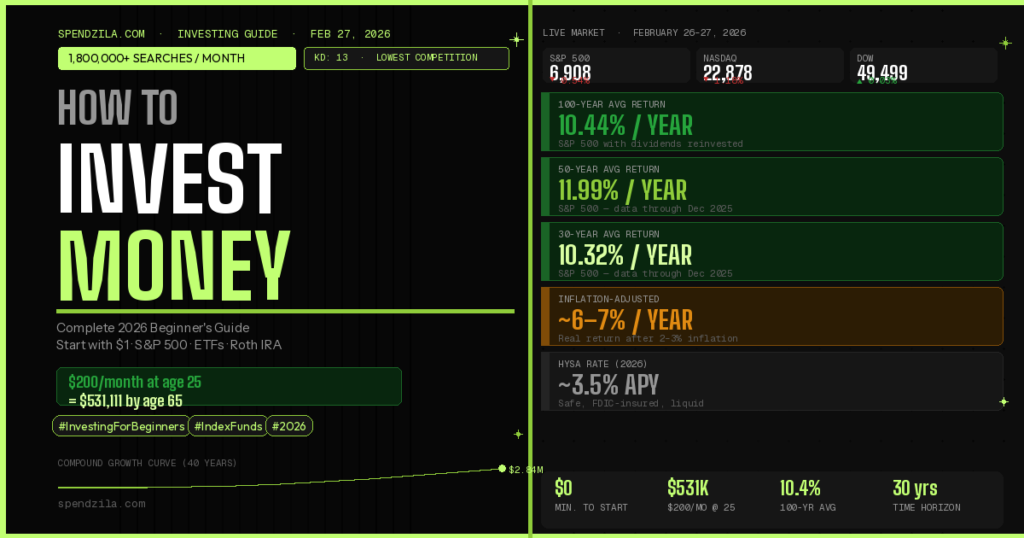

Open Free Tools →The S&P 500 closed at 6,908 on February 26, 2026 — down nearly 1% as Nvidia’s post-earnings slump rattled AI stocks and spooked beginners watching their first accounts drop. If you’ve been thinking about investing but haven’t started yet, or if you started and you’re now confused and nervous, this guide is for you.

Learning how to invest money is the single highest-impact financial skill you can build. A 25-year-old who invests just $200/month in a diversified index fund earning the S&P 500’s 100-year average of 10.4% annually could reach over $500,000 by age 65. Wait until 35 to start, and that number drops by more than half. The math is unforgiving — but it works in your favor if you start now.

This complete beginner’s guide covers everything: how investing works, the best account types, the best investments for beginners in 2026, how much you need to start, and a step-by-step action plan to open your first account today.

📈 S&P 500: 6,908.86 (52-week range: 4,835 – 7,002)

📉 Nasdaq: 22,878.38 — down 1.18% (Nvidia/AI sector volatility)

📈 Dow Jones: 49,499.20

💡 Historical context: S&P 500 has returned an average 10.4%/year over 100 years — short-term dips like today are normal. Long-term investors don’t react to them.

Most people understand that investing is important — but most people also keep putting it off. Here’s why delaying costs you more than any market drop ever will:

| Start Age | Monthly Investment | Total Contributed | Value at Age 65 (10% avg) | Gained from Growth |

|---|---|---|---|---|

| Age 25 | $200/mo | $96,000 | $531,111 | $435,111 |

| Age 30 | $200/mo | $84,000 | $325,783 | $241,783 |

| Age 35 | $200/mo | $72,000 | $195,989 | $123,989 |

| Age 40 | $200/mo | $60,000 | $114,780 | $54,780 |

*Assumes 10% average annual return (S&P 500 100-year historical average with dividends reinvested). For illustration only. Actual returns will vary.

There’s a second reason to invest now: inflation. Money sitting in a checking account loses about 2–3% of its purchasing power every year. At a 2.4% inflation rate (PCE forecast for 2026), $10,000 today becomes the equivalent of $7,610 in purchasing power in just 10 years if you don’t invest it. Investing isn’t just about getting rich — it’s about not getting poorer.

Investing means putting money into assets — stocks, bonds, funds, real estate — with the expectation they’ll grow in value over time. You make money in two ways: price appreciation (the asset goes up in value) and income (dividends, interest payments).

| Asset Class | What It Is | Historical Return | Risk Level | Best For |

|---|---|---|---|---|

| Stocks / Equities | Ownership shares of companies | ~10% annually (S&P 500) | High short-term | Long-term wealth building (5+ yrs) |

| Bonds | Loans to governments or corporations | 3–5% historically | Medium | Stability, income, near-retirement |

| Index Funds / ETFs | Basket of stocks tracking an index | ~10% (mirrors S&P 500) | Medium-High | Best for most beginners |

| Cash / HYSAs / CDs | Savings accounts, certificates of deposit | 3.5%–4.9% (2026) | Very Low | Emergency fund, short-term goals |

| Real Estate / REITs | Property or real estate investment trusts | 8–10% historically | Medium-High | Income + diversification |

Before you put a dollar into the market, check off these three items. Skipping them is the #1 beginner mistake:

Your emergency fund is your investment armor. Without it, a job loss or unexpected car repair forces you to sell your investments at the worst possible time — usually during a market dip. Calculate your monthly essential expenses (rent, food, transportation, insurance, minimum debt payments) and multiply by three. That total belongs in a high-yield savings account (HYSA) earning 3.5%+ in 2026 — liquid, safe, and working for you until needed. Only invest money you won’t need for at least 5 years. See our guide: How to Save Money Fast.

Any debt above 7–8% APR is earning your creditors more than the stock market earns you. Paying off a 24% APR credit card is a guaranteed 24% return — the stock market can’t beat that with certainty. Pay off high-interest debt first. The exception: your employer-matched 401(k) contribution — always capture 100% of any employer match before paying extra debt. A 50–100% guaranteed return on your 401(k) match beats any debt payoff math. See: Debt Consolidation Guide.

Your investment timeline determines everything else:

Where you invest matters as much as what you invest in. The right account type saves you thousands in taxes:

| Account Type | Tax Benefit | 2026 Contribution Limit | Withdrawal Rules | Best For |

|---|---|---|---|---|

| 401(k) / 403(b) | Pre-tax contributions, tax-deferred growth | $23,500 ($31,000 if 50+) | Penalty before 59½ (exceptions exist) | START HERE if employer matches |

| Roth IRA | After-tax now → 100% tax-free growth + withdrawals | $7,000 ($8,000 if 50+) | Contributions anytime; earnings after 59½ + 5 yrs | Best for young / lower-income investors |

| Traditional IRA | Possible pre-tax deduction; tax-deferred growth | $7,000 ($8,000 if 50+) | Taxed at withdrawal; required min. distributions at 73 | Higher earners expecting lower income in retirement |

| Taxable Brokerage | None — but no contribution limits | Unlimited | Anytime — capital gains tax applies on profits | After maxing tax-advantaged accounts; any goal |

| HSA (Health Savings Account) | Triple tax advantage — best tax deal in investing | $4,300 individual / $8,550 family | Medical anytime tax-free; non-medical after 65 | Anyone with a high-deductible health plan |

Follow this sequence to maximize every dollar’s tax efficiency:

| Investment | 2026 Return/Rate | Risk | Min. to Start | Verdict |

|---|---|---|---|---|

| S&P 500 Index Fund | ~10% long-term avg | Medium-High | $1–$5 (fractional) | 🏆 #1 for beginners |

| Total Market ETF (VTI) | ~10% long-term avg | Medium-High | $1 (fractional) | 🏆 #1 alternative |

| High-Yield Savings Account | ~3.5% APY (2026) | None (FDIC insured) | $0–$1 | ✅ Best for emergency fund |

| Treasury Bills/ETFs | 3.45%–4.9% (2026) | None (US govt backed) | $100 (TreasuryDirect) or $1 ETF | ✅ Best for 1–2 yr goals |

| Target-Date Fund | Varies by allocation | Adjusts automatically | $1,000 (some funds) | ✅ Best hands-off 401(k) pick |

| Dividend Stocks / ETFs | 6–9% total return + income | Medium | $1 (fractional) | ⚠️ Good after mastering basics |

| Individual Stocks | Highly variable | High | $1 (fractional) | ⚠️ Only with research + patience |

| Cryptocurrency | Highly speculative | Very High | $1 | ❌ Not for beginners — speculative |

An index fund is a type of investment fund that tracks a market index — most commonly the S&P 500. Instead of trying to pick individual winners, you buy the entire index. When you own an S&P 500 index fund, you own a tiny slice of all 500 of the largest US companies simultaneously.

| Fund | Tracks | Expense Ratio | Where to Buy |

|---|---|---|---|

| VOO (Vanguard S&P 500 ETF) | S&P 500 | 0.03% | Any brokerage |

| IVV (iShares Core S&P 500) | S&P 500 | 0.03% | Any brokerage |

| SWPPX (Schwab S&P 500 Index Fund) | S&P 500 | 0.02% | Schwab |

| VTI (Vanguard Total Market ETF) | Total US Stock Market | 0.03% | Any brokerage |

| VXUS (Vanguard International ETF) | International stocks (ex-US) | 0.07% | Any brokerage (add for diversification) |

The short answer: $0. In 2026, every major brokerage lets you open an account with no minimum balance. Most allow fractional share investing — meaning you can buy a $1 slice of any stock or ETF. Here’s what different starting amounts realistically look like:

| Starting Amount | What You Can Do | 10-Year Value (adding $0 more) | 30-Year Value (adding $0 more) |

|---|---|---|---|

| $5 | Open Schwab, buy fractional VOO | $12.97 | $87.25 |

| $100 | Full ETF share + start habit | $259.37 | $1,744.94 |

| $1,000 | Diversified portfolio, multiple ETFs | $2,593.74 | $17,449.40 |

| $5,000 | Strong foundation, multiple asset classes | $12,968.71 | $87,247.01 |

| $10,000 | Full beginner portfolio | $25,937.42 | $174,494.02 |

*Assumes 10% average annual return with no additional contributions. For illustration only.

Compound interest means you earn returns not just on your original investment, but on all your previous returns too. It creates a snowball effect that becomes almost unbelievable over 30–40 years.

| Age | Total Contributed | Account Value | Growth from Compounding |

|---|---|---|---|

| 35 | $60,000 | $95,625 | $35,625 |

| 45 | $120,000 | $347,758 | $227,758 |

| 55 | $180,000 | $1,027,726 | $847,726 |

| 65 | $240,000 | $2,839,934 | $2,599,934 |

| Brokerage | Account Min. | Commissions | Fractional Shares | Best For |

|---|---|---|---|---|

| Charles Schwab | $0 | $0 | Yes (from $5) | 🏆 #1 Pick (Feb 2026) |

| Fidelity | $0 | $0 | Yes (from $1) | Best education + tools + IRA options |

| Vanguard | $0 | $0 | Yes (ETFs) | Best for long-term index fund investing |

| Robinhood | $0 | $0 | Yes (from $1) | Simplest app for mobile-first beginners |

| SoFi Invest | $0 | $0 | Yes | Best all-in-one (banking + investing) |

| Betterment | $0 | 0.25%/yr | Yes (automated) | Best robo-advisor for hands-off investing |

For most beginners: Charles Schwab, Fidelity, or Vanguard. All charge $0 commissions and $0 minimums. Go to their website and click “Open an Account.”

If your employer offers a 401(k) match, maximize that first through your HR department — not through this brokerage. For your personal brokerage account: choose Roth IRA if you’re under 50 and your income qualifies (under $161,000 single / $240,000 married for 2026). Otherwise, choose a taxable brokerage account.

You’ll need: Social Security Number, government-issued ID, employer name and address, bank account information for funding. Most brokerages approve accounts within minutes.

Link your bank account and transfer your first deposit. Most brokerages process transfers in 1–3 business days. Schwab, Fidelity and Robinhood let you begin trading immediately with “instant deposits” of up to $1,000.

Search for VOO (Vanguard S&P 500 ETF) or VTI (Vanguard Total Market ETF). Select “Buy,” enter the dollar amount you want to invest (fractional shares work), and confirm. That’s it. You’re now an investor.

The most powerful move: automate a monthly transfer from your bank to your investment account — even $50 or $100. Then set up automatic investing in your chosen index fund. You’ll never think about it again, and compound growth does the work.

The S&P 500 dropped 0.54% yesterday. Nvidia fell 5.55%. The Nasdaq dropped 1.18%. Beginners panic. Long-term investors do nothing — and that’s exactly right.

The best time to invest is when you have money. The second-best time is right now. Research consistently shows that even investing at market peaks beats waiting — because more time in the market always wins over perfect timing. The 10 best days in the market over any 20-year period account for over 50% of total returns. Most of those days happen right after crashes, when beginners have already sold.

A 1% annual fee seems tiny — but on a $100,000 portfolio earning 10%, a 1% fee costs you $80,000 over 30 years versus a 0.03% index fund. Always check the expense ratio before buying any fund. Index funds from Vanguard, Schwab, and Fidelity charge 0.015–0.03% — essentially free.

Nvidia fell 5.55% in a single day on February 26, 2026, wiping billions in market cap despite beating earnings expectations. Individual stocks — even great companies — are volatile and unpredictable. Diversification across hundreds of companies via index funds eliminates this risk entirely.

This is the single most expensive mistake investors make. Studies consistently show that the average investor earns far less than the market average because they sell during drops and buy back in during rallies — the exact opposite of what works. Automate your investing, then ignore the noise.

A 24% APR credit card guaranteed return from paying off debt beats the stock market’s ~10% average return. Always pay off debt above 8% APR before investing beyond your employer 401(k) match. See: Debt Consolidation Guide.

A Roth IRA grows 100% tax-free. A 401(k) reduces your taxable income this year. Both are free money from the government that most beginners leave on the table by investing in a regular brokerage account first. Max tax-advantaged accounts before taxable accounts — always.

Daily checking creates emotional volatility that leads to bad decisions. Set up automatic investing, choose a quarterly review schedule, and let compound growth work. The best investors check their portfolios less, not more.

Open a free brokerage account at Charles Schwab, Fidelity, or Robinhood — all require $0 minimum. Enable fractional share investing and buy a slice of VOO or VTI for as little as $1–$5. Set up an automatic monthly contribution of whatever you can afford — $25, $50, $100. The amount matters less than the habit. Start today with whatever you have and increase contributions as your income grows. Use our guide to save money fast to free up more to invest each month.

For most beginners, a single S&P 500 index fund (like VOO or SWPPX) is all you need. It gives you instant ownership of 500 major US companies, charges near-zero fees, and historically returns ~10% annually. Once you’re comfortable, you can add a total international ETF (VXUS) for global diversification. Avoid individual stocks, crypto, and complex products until you’ve understood the basics and built your emergency fund first.

For long-term investors (5+ year horizon), there’s no wrong time to start investing in diversified index funds. The S&P 500 at 6,908 may seem “high,” but the same concern has been raised at every level — 1,000, 2,000, 3,000, 5,000 — and long-term investors who bought at each of those “high” levels have all made money. Short-term drops (like today’s 0.54% decline) are irrelevant over a 20-year investing horizon. If you’re investing for retirement in 20+ years, the best action today is the same as any other day: invest consistently in index funds and don’t react to short-term news.

A Roth IRA is a retirement account where you contribute after-tax money, and all future growth and withdrawals are 100% tax-free. You can contribute up to $7,000 per year ($8,000 if 50+) in 2026, and income limits apply. For young or lower-income investors, this is often the best investment account available — decades of compound growth accumulating completely tax-free is an extraordinary advantage. Open a Roth IRA at Fidelity, Schwab, or Vanguard immediately if you’re eligible (income under $161,000 single / $240,000 married for 2026).

The Ramsey framework suggests investing 15% of gross income for retirement (after securing your full employer 401(k) match and building your emergency fund). For perspective: 15% of a $60,000 salary is $750/month. If that seems like a lot, start with what you can — even $100/month invested at 25 becomes over $265,000 by 65 at 10% returns. The most important thing is to start something, then increase the amount as your income grows. Use the 50/30/20 rule to allocate 20% of income to savings and investing.

If you’re in diversified index funds and don’t sell, a market crash affects your paper value temporarily but doesn’t permanently destroy wealth. Every major crash in history — 1929, 1987, 2000, 2008, 2020 — has been followed by a full recovery and new all-time highs. The S&P 500 fell ~50% in 2008–2009, then went on to gain over 600% through 2026. Investors who held through the crash are far wealthier than those who sold. The real danger of a crash is panic-selling at the bottom. Avoid that one mistake and long-term investors consistently win.

Both can build serious wealth, but stocks (via index funds) are better for most beginners for three reasons: they require zero specialized knowledge, start with $1 instead of a 10–20% down payment, and are fully liquid (sell anytime). Real estate offers leverage, tangible assets, and rental income but requires significant capital, management, and expertise. Once you have a solid investment foundation (maxed Roth IRA, 401(k) contributions), real estate via REITs (Real Estate Investment Trusts) or direct property investment is an excellent diversification step.

For most beginner investors using simple index funds through a Roth IRA or 401(k), a financial advisor is not necessary. Index fund investing is genuinely simple once you understand the basics. Where advisors add real value: complex tax situations, estate planning, business owner finances, or investors with very large portfolios who want comprehensive planning. If you do use an advisor, look for a fee-only fiduciary (legally required to act in your interest) rather than a commission-based advisor who earns money from the products they sell you.

The stock market can go down in any given day, month, or even year. But over any 15-year period in US stock market history, a diversified investment has never resulted in a loss. Short-term: you might be up or down 20–30%. Medium-term (3–5 years): likely positive, not guaranteed. Long-term (10+ years): historically, always positive in the US market. Investing is a long-term game — the people who “make money fast” are mostly taking outsized risks or getting lucky. The reliable path is consistent investment over decades.

The most important investing decision you’ll make isn’t which stock to pick or whether the market is too high — it’s whether you start today or keep waiting. The math is clear: starting 10 years earlier on the same $200/month investment creates $335,000 more in wealth. Today’s market dip is irrelevant to someone investing for 30 years.

Your complete action plan:

Use our 50/30/20 budget rule to structure your income so investing becomes automatic. Track your credit score at What Is a Good Credit Score — a strong score unlocks better rates on every financial product you’ll ever need. And if you’re carrying high-interest debt, tackle it first with our Debt Consolidation Guide.

💳 Build Credit While You Build Wealth

A strong credit score (760+) unlocks the lowest mortgage rates — potentially saving $100,000+ on your home loan. A $0-fee cash back card used responsibly is one of the fastest ways to build it while earning rewards on every purchase.

Be the first to leave a comment!

Leave a Comment