Use Spendzila's free calculators to apply what you learn in this article instantly.

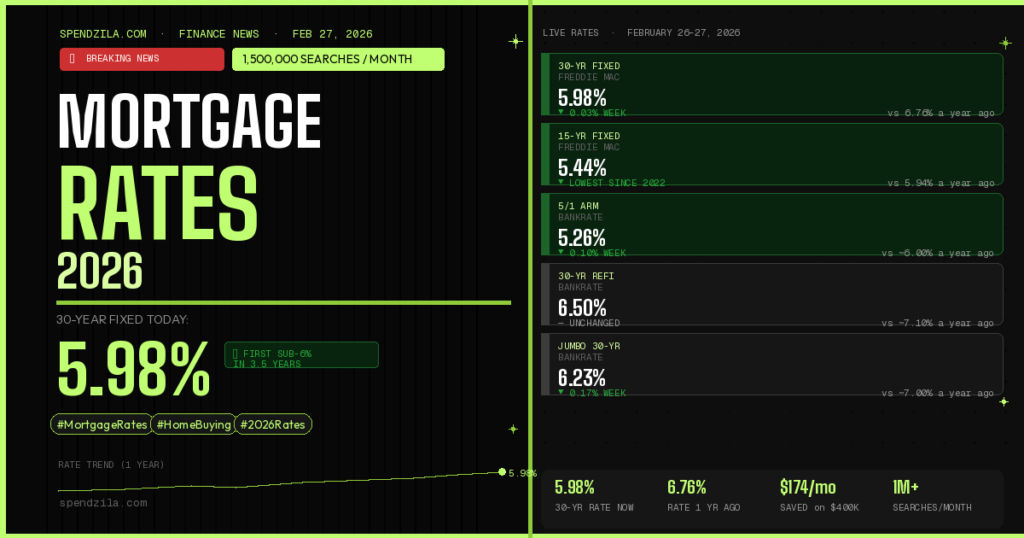

Open Free Tools →Something major just happened in the mortgage market. As of February 26, 2026, the 30-year fixed mortgage rate fell to 5.98% — the first time it has dropped below 6% in three and a half years, according to Freddie Mac’s official weekly survey. If you’ve been waiting for rates to come down before buying a home or refinancing, that moment may be here.

In this complete guide, we cover today’s live mortgage rates for every loan type, the 2026 rate forecast from major institutions, how rates are determined, what different rates mean for your actual monthly payment, and the exact steps to qualify for the lowest possible rate.

🏠 30-year fixed (Freddie Mac): 5.98% — first sub-6% reading in 3.5 years

🏠 15-year fixed (Freddie Mac): 5.44%

🔄 30-year refinance (Bankrate): 6.50%

📉 1 year ago: 6.76% — you’re now paying 0.78% less than a year ago

⚠️ Forecast: MBA + Fannie Mae expect rates to hover near 6% through 2026 — no dramatic cuts expected

Mortgage rates vary across lenders and data sources. Here’s the complete picture from the most trusted rate sources as of this week:

| Loan Type | Rate (Freddie Mac) | Rate (Bankrate) | Rate (NerdWallet APR) | 1 Year Ago |

|---|---|---|---|---|

| 30-Year Fixed | 5.98% ⬇️ | 6.05% | 5.79% APR | 6.76% |

| 15-Year Fixed | 5.44% | 5.54% | 5.41% APR | 5.94% |

| 5/1 ARM | — | 5.26% | 6.29% APR | ~6.00% |

| 30-Year Refinance | — | 6.50% | — | ~7.10% |

| 15-Year Refinance | — | 5.82% | — | ~6.50% |

| Jumbo 30-Year | — | 6.23% | — | ~7.00% |

Data as of February 26, 2026. Freddie Mac data from weekly PMMS survey (released Thursdays). Bankrate reflects daily survey of major lenders. Rates change daily — always verify directly with lenders before making decisions. APR includes fees and points.

A mortgage rate is the interest rate a lender charges you to borrow money to buy a home. It’s expressed as an annual percentage and determines how much of your monthly payment goes toward interest versus paying down the loan principal.

When comparing mortgage offers, you’ll see two numbers:

| Type | How It Works | Feb 2026 Rate | Best For |

|---|---|---|---|

| Fixed-Rate (30-yr) | Rate locked for entire 30 years — payment never changes | 5.98% | Stability seekers, long-term owners |

| Fixed-Rate (15-yr) | Lower rate, higher payment, paid off in half the time | 5.44% | Borrowers who can afford higher monthly payment |

| 5/1 ARM | Fixed for 5 years, then adjusts annually to market rate | 5.26% | Those selling or refinancing within 5 years |

Your credit score is the single biggest factor determining your mortgage rate. Here’s exactly what borrowers pay at different credit tiers in February 2026:

| FICO Score | Credit Tier | Typical 30-yr Rate | Monthly Payment* | Total Interest Paid* |

|---|---|---|---|---|

| 760–850 | Exceptional | 5.70%–6.00% | $1,166–$1,199 | $219,760–$231,640 |

| 720–759 | Very Good | 6.00%–6.40% | $1,199–$1,255 | $231,640–$251,800 |

| 680–719 | Good | 6.40%–6.90% | $1,255–$1,327 | $251,800–$277,720 |

| 640–679 | Fair | 6.90%–7.60% | $1,327–$1,435 | $277,720–$316,600 |

| 580–639 | Poor (FHA only) | 7.60%–8.50%+ | $1,435–$1,573+ | $316,600–$365,880+ |

*Based on $200,000 loan amount, 30-year fixed-rate mortgage, principal + interest only. February 2026 rate estimates.

Here’s what the current historic 5.98% rate actually costs at different home price levels, with 20% down payment:

| Home Price | 20% Down | Loan Amount | Monthly P&I at 5.98% | vs. 6.76% (1 yr ago) |

|---|---|---|---|---|

| $200,000 | $40,000 | $160,000 | $958/mo | Save $87/mo |

| $300,000 | $60,000 | $240,000 | $1,437/mo | Save $130/mo |

| $400,000 | $80,000 | $320,000 | $1,916/mo | Save $174/mo |

| $500,000 | $100,000 | $400,000 | $2,395/mo | Save $217/mo |

| $750,000 | $150,000 | $600,000 | $3,593/mo | Save $326/mo |

Monthly payments above are principal and interest only. Your actual payment will include property taxes, homeowners insurance, and PMI if your down payment is below 20%. Use these numbers as a starting point.

The choice between a 30-year and 15-year mortgage is one of the most important financial decisions in homebuying. Here’s the complete breakdown:

| Factor | 30-Year Fixed (5.98%) | 15-Year Fixed (5.44%) |

|---|---|---|

| Rate (Feb 2026) | 5.98% | 5.44% (0.54% lower) |

| Monthly Payment on $300K loan | $1,796 | $2,454 ($658 more) |

| Total Interest on $300K | $346,560 | $141,720 |

| Interest Savings (15-yr) | — | $204,840 saved |

| Equity buildup | Slower — mostly interest early on | Faster — more principal paid monthly |

| Best for | Lower monthly payment, flexibility, first-time buyers | Saving maximum interest, payoff speed, strong income |

The type of mortgage you get dramatically affects your rate. Here’s how all major loan types compare:

| Loan Type | Approx. Rate (Feb 2026) | Min. Down Payment | Min. Credit Score | Best For |

|---|---|---|---|---|

| Conventional 30-yr | 5.98%–6.11% | 3%–20% | 620 | Good-excellent credit, standard purchase |

| Conventional 15-yr | 5.44%–5.54% | 3%–20% | 620 | Saving maximum interest, faster payoff |

| FHA 30-yr | ~5.65%–5.85% | 3.5% (580+ score) | 500 (10% down) / 580 (3.5% down) | Lower credit, lower down payment |

| VA 30-yr | ~5.45%–5.65% | 0% | None (lender may require 580+) | Veterans, active military, surviving spouses |

| USDA 30-yr | ~5.60%–5.80% | 0% | 640 | Rural area buyers, income limits apply |

| Jumbo 30-yr | 6.23%–6.40% | 10%–20% | 700+ | Loans above $806,500 (2026 conforming limit) |

One important 2026 tax change affects home buyers: thanks to the One Big Beautiful Bill Act (OBBBA), private mortgage insurance (PMI) premiums are tax-deductible again in 2026 — with an income phase-out between $100K–$110K AGI. This means buyers putting down less than 20% can now deduct their PMI costs, reducing the effective cost of lower-down-payment mortgages. Also, the SALT cap jumped to $40,000 for married couples, dramatically increasing mortgage interest deduction benefits for many homeowners.

After dropping below 6% for the first time since September 2022, where are mortgage rates headed for the rest of 2026?

| Institution | 30-Year Rate Forecast (2026 Avg) | Key Assumption |

|---|---|---|

| Mortgage Bankers Association (MBA) | ~6.10% through 2026 | Fed holds rates steady most of year |

| Fannie Mae | ~6.00% through year-end | Gradual rate stabilization |

| Zillow Research | 5.76%–6.10% range | Rates at new low on Feb 24 |

| Freddie Mac (current) | 5.98% as of Feb 26 | Live data — first sub-6% in 3.5 years |

Several factors pushed mortgage rates to their lowest level since late 2022:

Unlikely in 2026 based on current forecasts. The MBA and Fannie Mae both see rates averaging near 6% through the year. A significant economic downturn or emergency Fed rate cuts could push rates lower, but experts note that pandemic-era rates of 2.5–3.5% were extraordinary outliers driven by emergency policy — not a baseline to expect to return to.

Mortgage rates are determined by two layers of factors: macroeconomic forces (which set the baseline) and personal financial factors (which determine what YOU specifically pay).

| Factor | Impact on Rates | 2026 Status |

|---|---|---|

| 10-Year Treasury Yield | Most direct — mortgage rates track this closely | Trending down in late Feb 2026 |

| Federal Reserve Policy | Influences short-term rates; Fed funds rate affects overall lending costs | Held steady; March meeting expected to hold again |

| Inflation | Higher inflation → higher rates; lower inflation → lower rates | Moderating, positive signal for rates |

| Economic Growth / Jobs | Strong economy → higher rates; weak economy → lower rates | Mixed signals — uncertainty keeping rates lower |

| Personal Factor | Impact | Optimal Level |

|---|---|---|

| Credit Score | Biggest personal factor — up to 1.5%+ rate difference | 760+ for best rates |

| Down Payment | 20%+ eliminates PMI; larger down payment = lower rate | 20%+ ideal; 10% acceptable |

| Loan-to-Value Ratio | Lower LTV = lower risk = lower rate | Below 80% LTV |

| Debt-to-Income Ratio | Lower DTI = better approval odds and potentially lower rate | Below 36%; max 43% for most loans |

A credit score jump from 680 to 760 can drop your mortgage rate by 0.5–1.5%, saving $50,000–$150,000 in interest on a typical mortgage. Steps to improve quickly: pay down credit card balances below 30% utilization, dispute any errors on your credit report (get free reports at AnnualCreditReport.com), and make zero new credit applications for 90 days before mortgage shopping. See: What Is a Good Credit Score?

Every 5% more you put down reduces your rate slightly and lowers your loan-to-value ratio. The magic threshold is 20% — at that point, you eliminate PMI (which adds 0.5–1.5% to your effective cost annually) and qualify for better rates. Even going from 5% to 10% down meaningfully improves your rate and reduces your monthly payment.

Research from the Consumer Financial Protection Bureau shows that getting just one additional mortgage quote saves the average borrower $1,500 over the loan life. Getting five quotes saves $3,000+. Rate differences of 0.5–1.0% between lenders for the same borrower are common. Compare: your local bank, a credit union, and 2–3 online lenders (Better.com, Rocket Mortgage, loanDepot). Pre-qualification is free and uses a soft credit pull that doesn’t affect your score.

One discount point = 1% of the loan amount paid upfront in exchange for a rate reduction of roughly 0.25%. On a $300,000 loan, one point costs $3,000 and saves about 0.25% annually. This “breaks even” in about 4–5 years. If you plan to stay in the home long-term, points are worth it. If you might sell or refinance within 5 years, skip them.

VA loans (for veterans) currently offer rates 0.25–0.50% lower than conventional loans with no down payment required — if you’re eligible, this is almost always the best option. FHA loans offer competitive rates for borrowers with lower credit scores. USDA loans serve rural buyers with 0% down at competitive rates. Don’t default to a conventional loan if a government-backed loan serves you better.

A rate lock guarantees your rate for 30–60 days while you complete the home purchase. Lock too early and you miss further drops; too late and you risk rates rising before closing. In the current environment (rates just hit a 3.5-year low), many experts suggest locking if you’re within 30 days of closing, while maintaining a float-down option if your lender offers one — this lets you capture a lower rate if rates drop further before you close.

Pay off any small loans or credit card balances before applying. Every $300/month you eliminate from your monthly debt payments improves your DTI significantly. Lenders want your total DTI (including the new mortgage payment) below 43% — ideally below 36%. See our guide on debt consolidation and saving money fast to prepare financially.

Pre-qualification is a soft estimate. Pre-approval involves a full credit check, income verification, and a conditional commitment from the lender — it shows sellers you’re a serious buyer AND gives you an accurate rate quote. In a competitive market, sellers consistently prefer pre-approved buyers. Pre-approval typically takes 1–3 days at most online lenders.

This is the question on every potential buyer’s mind. Here’s the honest answer based on the current data:

With the 30-year rate at 5.98% and refinance rates at 6.50%, refinancing makes sense for a specific group of homeowners. The general rule: refinancing typically makes sense if you can reduce your rate by at least 0.75–1.0 percentage points and plan to stay in the home long enough to recover closing costs (typically $3,000–$6,000).

| Your Current Rate | Refi Rate Available | Monthly Savings on $300K | Break-Even Period |

|---|---|---|---|

| 7.50% | 6.50% | ~$200/month | ~20 months ✅ Excellent |

| 7.00% | 6.50% | ~$100/month | ~40 months ✅ Good |

| 6.75% | 6.50% | ~$50/month | ~80 months ⚠️ Marginal |

| 6.50% or below | 6.50% | $0 or negative | ❌ Not worth it |

Refinancing is most attractive for: Homeowners who bought in 2023–2024 with rates of 7–8%+. A drop from 7.50% to 6.50% on a $300,000 mortgage saves $200/month — that’s $2,400/year and you recoup closing costs in under 2 years.

As of February 26–27, 2026, the average 30-year fixed mortgage rate is approximately 5.98% according to Freddie Mac’s weekly PMMS survey — the first time in three and a half years the rate has been below 6%. Bankrate’s daily survey shows 6.05%, while NerdWallet’s APR data shows 5.79%. The variation reflects different methodologies and whether fees are included. Your actual rate will depend on your credit score, down payment, loan type, and lender.

Most major institutions predict 30-year mortgage rates will hover near 6% throughout 2026. The Mortgage Bankers Association forecasts approximately 6.10%, while Fannie Mae expects rates near 6.00% through year-end. Rates could fall further if the Federal Reserve cuts its benchmark rate or if economic data weakens significantly. However, a return to pandemic-era lows below 4% is not expected by any major forecaster in 2026.

The minimum credit score depends on the loan type. Conventional loans typically require a minimum score of 620. FHA loans accept scores as low as 500 (with 10% down) or 580 (with 3.5% down). VA and USDA loans have no official minimum but most lenders require 580–620. However, the best mortgage rates — including the current advertised 5.98% — are generally reserved for borrowers with credit scores of 760 or higher. Every tier below that typically adds 0.1–0.5% to your rate.

On a $300,000 mortgage over 30 years, a 1% rate difference equals approximately $175/month in payment difference and over $63,000 in total interest over the life of the loan. On a $500,000 mortgage, the same 1% difference means about $292/month and $105,000 total. This is why shopping multiple lenders and improving your credit score matters so much — even a 0.5% better rate saves tens of thousands of dollars.

A 15-year mortgage (currently ~5.44%) gives you a lower rate and saves enormous interest — on a $300,000 loan, you’d pay $204,840 less in interest than the 30-year option. But the monthly payment is $658 higher. The 30-year (5.98%) offers lower required payments and flexibility. The best strategy for many borrowers is a 30-year mortgage with aggressive extra principal payments whenever possible, giving the flexibility of a 30-year payment while building equity at a 15-year pace.

Once a lender issues you a loan approval, you can request a rate lock — typically for 30, 45, or 60 days (longer locks may cost extra). The lock guarantees your rate during that window while you finalize the purchase. Ask your lender about “float-down” options — some lenders allow you to capture a lower rate if rates drop after your lock, for a small fee. In today’s environment with rates at a 3.5-year low, locking soon after approval is generally wise.

The mortgage interest rate is the base cost of borrowing — it’s used to calculate your monthly principal and interest payment. The APR (Annual Percentage Rate) includes the interest rate plus all lender fees (origination charges, discount points, broker fees, mortgage insurance) expressed as a yearly percentage. APR is always higher than the interest rate and is the most accurate way to compare loan offers from different lenders. When lenders advertise a 5.79% rate, the actual APR you pay may be 6.0–6.2% once fees are included.

Refinancing makes financial sense if you can reduce your rate by at least 0.75–1.0 percentage points AND plan to stay in your home long enough to recoup the closing costs (typically $3,000–$6,000). If you bought or last refinanced when rates were 7–8% in 2023–2024, today’s rates of 6.5% on refinances represent a meaningful opportunity. Calculate your break-even point: divide your estimated closing costs by your monthly savings to find how many months until you recoup the cost.

Private Mortgage Insurance (PMI) is required when you put less than 20% down on a conventional loan. It protects the lender — not you — and typically costs 0.5–1.5% of the loan amount annually (added to your monthly payment). Good news for 2026: PMI premiums are now tax-deductible again under the OBBBA (income limits apply). You can request PMI removal once your loan-to-value ratio reaches 80% (either through payments or home appreciation). Under federal law (Homeowners Protection Act), lenders must automatically cancel PMI when your LTV reaches 78%.

The conforming loan limit — the maximum loan amount eligible for conventional financing backed by Fannie Mae or Freddie Mac — is $806,500 for most of the US in 2026, with higher limits in high-cost areas (up to $1,209,750 in areas like San Francisco and New York City). Loans above these limits are “jumbo” mortgages, which typically carry higher rates and stricter qualification requirements.

Mortgage rates just dropped below 6% for the first time in 3.5 years — and that’s genuinely significant news for millions of Americans who have been waiting on the sidelines. The 30-year fixed rate at 5.98% represents real savings of $87–$326/month compared to just one year ago, depending on your home price.

What you should do right now:

The best mortgage rate is the one you qualify for today — not the theoretical bottom you might catch someday. With rates at their lowest in years and spring homebuying season approaching, the window to act is genuinely here.

💳 Also: Build Your Credit to Get the Best Rate

A 760+ credit score gets you the best mortgage rates — potentially saving $100,000+ over 30 years. A cash back credit card used responsibly is one of the fastest ways to build credit. See our $0-fee picks.

Be the first to leave a comment!

Leave a Comment