Use Spendzila's free calculators to apply what you learn in this article instantly.

Open Free Tools →A personal loan lets you borrow a fixed amount of money, repay it in predictable monthly installments, and use it for almost anything — debt consolidation, home improvement, medical bills, or major life expenses. With 25.9 million Americans currently holding personal loans and average rates sitting at 12.26% APR in February 2026, knowing how to find the best deal could save you thousands of dollars.

This complete guide covers everything: how personal loans work, current 2026 rates, what you need to qualify, the 8 best lenders compared side-by-side, and a step-by-step application guide so you know exactly what to expect.

📊 Avg rate (all lenders): 12.26% APR

🏦 Best available rate: 6.49% APR (excellent credit, online lenders)

📈 Fed funds rate: 3.5–3.75% (held steady, no cut in Jan 2026)

💡 Bottom line: Rates are elevated but competitive. Shop 3+ lenders — the difference can be 5+ percentage points on the same borrower.

A personal loan is a fixed amount of money you borrow from a bank, credit union, or online lender and repay — with interest — in equal monthly installments over a set period, typically 2 to 7 years.

Unlike a mortgage or auto loan, most personal loans are unsecured — meaning no collateral required. The lender evaluates your creditworthiness, income, and debt load, then decides whether to lend and at what rate. The better your credit and financial profile, the lower your rate.

| Feature | Details |

|---|---|

| Loan amounts | $1,000 – $100,000 (varies by lender) |

| Repayment terms | 2 – 7 years (some lenders offer up to 12 years) |

| Interest rates | 6.49% – 35.99% APR (Feb 2026 range) |

| Collateral required | No (unsecured) for most — or optional to lower your rate |

| Funding speed | As fast as same day — typically 1–5 business days |

| Minimum credit score | 300+ (Upstart) to 660+ (best lenders) |

Understanding the mechanics of a personal loan helps you borrow smarter:

You submit an application — usually online in 10–15 minutes. The lender does a soft inquiry (pre-qualification, no credit impact) to give you rate estimates, then a hard inquiry if you formally apply. You receive a loan offer specifying amount, rate, term, monthly payment, and any fees.

Once approved, the lender deposits the full loan amount into your bank account — typically within 1–5 business days. Some lenders like Rocket Loans and Best Egg offer same-day or next-day funding. If you’re using it for debt consolidation, some lenders pay your creditors directly.

Every month, you pay a fixed amount that includes both principal and interest. Unlike a credit card, your payment never changes and you know exactly when the loan ends. Setting up autopay (0.25–0.50% rate discount at most lenders) ensures you never miss a payment.

Your true cost includes:

| Type | How It Works | Best For | Rate Impact |

|---|---|---|---|

| Unsecured Personal Loan | No collateral; approved based on credit + income | Most borrowers; all purposes | Standard rates |

| Secured Personal Loan | Backed by collateral (savings, car, etc.) | Borrowers with limited credit | Lower rates (1–3% less) |

| Debt Consolidation Loan | Personal loan specifically to pay off other debts | High-interest credit card holders | Same as unsecured |

| Co-signed Loan | Second person guarantees the loan | Bad credit borrowers with a co-signer | Co-signer’s credit applies |

| Fixed-Rate Loan | Rate stays the same for full term | Predictable budgeters; most people | Standard; no change risk |

| Variable-Rate Loan | Rate changes with market index | Short-term borrowers in falling-rate environment | Can be lower initially; risk of rising |

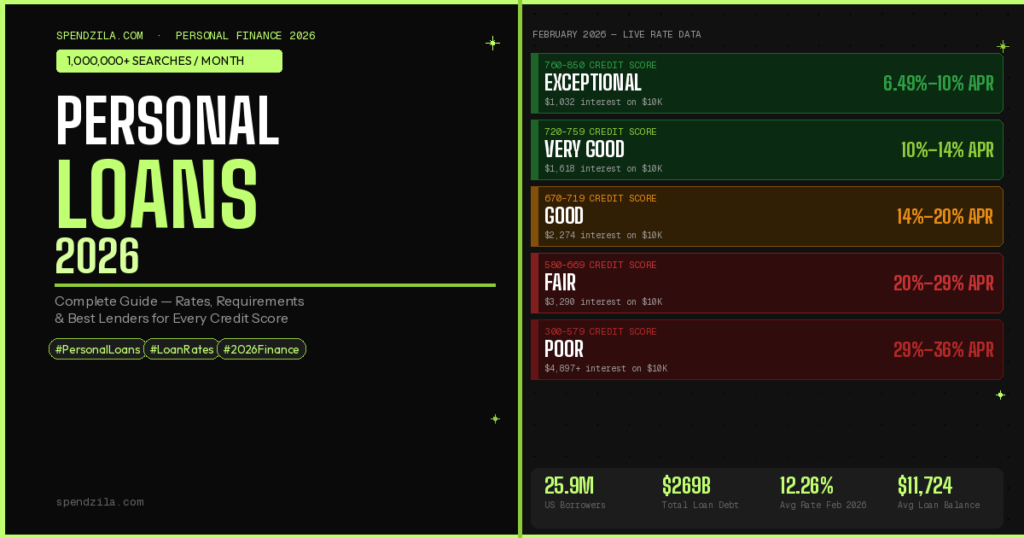

Personal loan rates vary widely based on your credit score, lender type, loan amount, and repayment term. Here’s the complete rate landscape as of February 2026:

| Lender Type | Average APR | Range | Note |

|---|---|---|---|

| Online lenders | Avg ~11–14% | 6.49%–35.99% | Widest range, most competitive for good credit |

| Credit unions | 10.64% | 7%–18% | Q4 2025 NCUA data; typically lowest average |

| Commercial banks | 12.06% | 8%–29% | Federal Reserve data, Q4 2025 |

| Overall average (all lenders) | 12.26% | 6.49%–35.99% | February 2026 |

| Credit Score Range | Rating | Typical APR Range | Interest on $10K/3-yr |

|---|---|---|---|

| 760–850 | Exceptional | 6.49%–10% | $1,032–$1,618 |

| 720–759 | Very Good | 10%–14% | $1,618–$2,274 |

| 670–719 | Good | 14%–20% | $2,274–$3,290 |

| 580–669 | Fair | 20%–29% | $3,290–$4,897 |

| 300–579 | Poor | 29%–35.99%+ | $4,897–$6,489+ |

Lenders evaluate five key factors. Understanding each helps you know where you stand before applying:

| Factor | Minimum to Qualify | Ideal for Best Rate | Weight |

|---|---|---|---|

| Credit Score | 580 (most lenders) | 720+ | 🔑 Most important |

| Annual Income | ~$20,000+ | $50,000+ | Very important |

| Debt-to-Income Ratio | Below 50% | Below 35% | Very important |

| Employment/Income Stability | Any regular income | 2+ years same employer | Moderate |

| Payment History | No recent bankruptcies | Zero missed payments in 12 months | Moderate |

We compared the top personal loan lenders on rates, fees, minimum credit scores, loan amounts, and funding speed. Here’s who wins for each type of borrower:

| Lender | APR Range | Loan Amount | Min. Credit | Fees | Funding | Best For |

|---|---|---|---|---|---|---|

| LightStream | 6.94%–25.29% | $5K–$100K | 660 | None | Same day | Lowest rates overall |

| SoFi | 8.99%–29.99% | $5K–$100K | 650 | None | 1–3 days | No fees + member benefits |

| Marcus by Goldman Sachs | 6.99%–24.99% | $3.5K–$40K | 660 | None | 1–4 days | Zero fees, trusted brand |

| Discover | 7.99%–24.99% | $2.5K–$40K | 660 | None | Next day | Debt consolidation (pays creditors directly) |

| Best Egg | 6.99%–35.99% | $2K–$50K | 600 | 0.99%–8.99% | 1–3 days | Fastest funding |

| Upstart | 7.80%–35.99% | $1K–$50K | 300 | 0%–12% | 1–3 days | Bad/limited credit |

| Achieve | 8.99%–35.99% | $5K–$50K | 620 | 1.99%–6.99% | 1–3 days | Fair credit + co-borrower option |

| PenFed Credit Union | 7.99%–17.99% | $600–$50K | 650 | None | 1–5 days | Credit union rates |

Personal loans are one of the most flexible financial products available — you can use them for almost any legal purpose. The most common uses in 2026:

| Use Case | % of Borrowers | Smart Move? |

|---|---|---|

| Debt consolidation | 51.0% | ✅ Yes — if rate is lower than current debts |

| Everyday bills / emergency expenses | 9.5% | ⚠️ OK short-term; build emergency fund to avoid |

| Home improvement | 6.9% | ✅ Yes — value-adding projects especially |

| Medical expenses | 5.4% | ✅ Yes — negotiate bill first, then use loan |

| Major purchases (appliances, car repair) | 4.8% | ✅ Yes — better than credit card interest |

| Wedding or vacation | ~3% | ⚠️ Think carefully — you’ll pay for years after the event |

| Business or investment | ~2% | ❌ Usually better options exist (SBA loans, investors) |

Most personal loans prohibit use for: college tuition (use student loans), down payment on a home (lenders require down payments come from your own assets), illegal activity, or business purchases at lenders who specifically exclude business use. Always read your loan agreement.

| Feature | Personal Loan | Credit Card | HELOC |

|---|---|---|---|

| Typical APR | 6.49%–35.99% | 19%–29% | 7%–10% |

| Fixed payments | ✅ Yes | ❌ Varies | ⚠️ Draw phase interest-only |

| Defined payoff date | ✅ Yes | ❌ No | ⚠️ Only in repayment phase |

| Collateral required | ❌ No | ❌ No | ✅ Home equity |

| Best for large amounts | Up to $100K | Up to $25K typically | Hundreds of thousands |

| Funding speed | 1–5 days | Instant (if card exists) | 2–6 weeks |

| Risk if you can’t pay | Credit damage | Credit damage | Lose your home |

Choose a personal loan when: You need $2,000–$50,000, want a fixed payoff date, and your credit qualifies you for a rate below your current credit card APR.

Choose a 0% balance transfer card when: Your debt is under $15,000, your credit score is 670+, and you can pay it off within the 0% intro period (12–21 months).

Choose a HELOC when: You own a home with equity, need a large amount, have stable income, and fully understand the foreclosure risk.

Check for free at Credit Karma (VantageScore 3.0) or AnnualCreditReport.com (free official FICO report). Your score determines which lenders will approve you and at what rate. If it’s below 620, consider improving it for 30–60 days before applying — even small improvements can save hundreds.

Be precise. Borrowing more than needed means paying more interest unnecessarily. Borrowing too little means a second application later (another hard inquiry). Include any fees in your calculation — if a lender charges a 5% origination fee on a $10,000 loan, you’ll only receive $9,500 but owe $10,000.

Every major lender now offers pre-qualification using a soft inquiry — zero impact on your credit score. Submit to at least three lenders simultaneously: LightStream, SoFi, and Marcus are a solid trio for good credit. This takes 10–15 minutes total and gives you real rate offers to compare.

A 7-year loan at 10% APR has a lower monthly payment than a 3-year loan at the same rate — but you’ll pay more than double the interest over the life of the loan. Always compare: Total Interest Paid = Total of All Payments − Loan Amount. Choose the shortest term you can comfortably afford.

Once you’ve chosen the best offer, complete the full application. This involves a hard credit inquiry (–5 to –10 points, temporary). Have all documents ready: ID, SSN, income proof, employer info. Most online lenders complete this in 24–48 hours.

Before accepting: check the APR (not just rate), total payback amount, origination fee, prepayment penalties, and monthly payment. Confirm everything matches the pre-qualification offer. If anything changed, ask why before signing.

Most lenders offer a 0.25%–0.50% APR discount for autopay enrollment. More importantly, autopay prevents missed payments which can cost you $25–$40 in fees and damage your credit score. Set it up on day one.

Here’s exactly what different loan amounts cost at current 2026 rates across three credit tiers:

| Loan Amount | Term | Excellent Credit (7%) | Good Credit (14%) | Fair Credit (24%) |

|---|---|---|---|---|

| $5,000 | 3 years | $155/mo — $578 interest | $171/mo — $1,148 interest | $196/mo — $2,063 interest |

| 5 years | $99/mo — $940 interest | $116/mo — $1,985 interest | $143/mo — $3,602 interest | |

| $10,000 | 3 years | $309/mo — $1,115 interest | $342/mo — $2,274 interest | $392/mo — $4,125 interest |

| 5 years | $198/mo — $1,880 interest | $233/mo — $3,970 interest | $285/mo — $7,117 interest | |

| $25,000 | 3 years | $772/mo — $2,788 interest | $854/mo — $5,685 interest | $979/mo — $10,313 interest |

| 5 years | $495/mo — $4,700 interest | $582/mo — $9,924 interest | $713/mo — $17,793 interest |

You’re in the best position. Start with LightStream and Marcus — both offer rates starting under 7% with no fees. Pre-qualify at both plus SoFi to compare. Avoid any lender charging origination fees above 2%; the math rarely works in your favor when no-fee lenders exist at competitive rates.

Your options are narrower but real. Upstart uses an AI-driven model that considers education and job history — not just credit score — which helps many fair-credit borrowers get better rates than traditional lenders offer. Achieve and Avant also serve this segment. Expect rates of 20–29%, and seriously consider whether improving your credit for 60–90 days before applying would dramatically change your rate.

Traditional unsecured personal loans are difficult to obtain. Options:

Even a 30–50 point improvement can drop your rate by 3–5 percentage points. Quick wins: pay down credit card balances (lowers utilization), dispute any errors on your credit report, and avoid any new credit inquiries for 90 days before applying. See our full guide: What Is a Good Credit Score?

Soft-inquiry pre-qualification means you can check your rate at 5 lenders in one afternoon with zero credit impact. Rate differences of 3–8% between lenders are common for the same borrower. This five-minute step can save you thousands.

Shorter terms (2–3 years) come with lower rates AND less total interest. If you can afford the higher monthly payment, always choose the shorter term. The difference between a 3-year and 7-year loan at the same rate is typically 50–100% more in total interest paid.

Most lenders offer a 0.25%–0.50% rate reduction for autopay enrollment — given automatically. On a $15,000 loan, that’s $200–$400 in savings over a 3-year term just for setting up automatic payments.

Pay off any small balances (store cards, medical bills, etc.) before applying to reduce your monthly debt obligations. A DTI drop from 45% to 38% can move you from a “borderline” to “qualified” borrower, unlocking better rates and higher approval amounts.

Banks and credit unions often offer 0.25–1% better rates to existing customers. Your credit union’s average rate is 10.64% APR vs. 12.06% at commercial banks — that’s meaningful savings, especially for larger loans.

Origination fees of 3–8% can wipe out any rate advantage. On a $20,000 loan, a 5% origination fee costs $1,000 upfront. Compare the effective APR (which includes fees) — not just the interest rate. LightStream, SoFi, Marcus, PenFed, and Discover all charge zero origination fees.

The average personal loan interest rate across all lenders in February 2026 is 12.26% APR. Credit unions average 10.64% APR, commercial banks average 12.06% APR, and online lenders range from 6.49% to 35.99% APR depending on your credit profile. Borrowers with excellent credit (760+) can find rates as low as 6.49–7.99% APR from top online lenders.

Most traditional lenders require a minimum credit score of 580–620, though you’ll need 660+ for competitive rates and 720+ for the lowest rates available. Upstart accepts borrowers with credit scores as low as 300 using an AI model that considers education and employment history. The higher your credit score, the more lenders will compete for your business — and the lower your rate.

Online lenders are the fastest: pre-qualification takes 2–5 minutes, formal approval comes in 24–48 hours, and most fund within 1–3 business days. Best Egg and Rocket Loans offer same-day or next-business-day funding in some cases. Banks and credit unions typically take 3–7 business days from application to funding.

Yes, though options are limited and rates are high. Upstart accepts borrowers with scores as low as 300 and evaluates your employment and education history. Secured personal loans (using savings or a vehicle as collateral) are another option. Many credit unions have credit-builder loan programs specifically for rebuilding credit. If your rate would be 29%+ APR, consider whether the loan is truly worth it — or whether improving your credit for 60–90 days first would dramatically lower your rate.

For amounts over $2,000 where you need more than 15–18 months to repay, a personal loan with a rate of 12–15% APR is almost always cheaper than a credit card at 20–29% APR. For amounts under $2,000 that you can pay within a 0% intro APR period (12–21 months), a balance transfer card wins. Personal loans also provide the psychological and mathematical benefit of a fixed payoff date — you know exactly when you’ll be debt-free.

Applying causes a temporary hard inquiry (–5 to –10 points). Opening a new account initially lowers your average account age. However, if you use the loan to pay off credit card debt, your credit utilization ratio drops significantly, which typically provides a net positive credit score impact within 1–2 billing cycles. After 6–12 months of on-time payments, most borrowers see their credit score higher than before they applied for the loan.

Most lenders — including SoFi, LightStream, Marcus, and Discover — charge no prepayment penalties. Paying early saves you interest, because you’re paying the principal down faster. However, always check your loan agreement first. Some lenders do charge prepayment fees, and the savings from early payoff must outweigh any fees charged.

Most lenders cap personal loans at $50,000–$100,000. LightStream and SoFi both offer up to $100,000. Maximum amounts depend heavily on your income and creditworthiness — lenders typically won’t approve loan amounts where the monthly payment would exceed 40–50% of your income. For borrowing needs above $100,000, home equity loans (if you own property) or business loans are more appropriate.

Personal loan proceeds are not taxable income — you don’t owe taxes on money you borrow. However, personal loan interest is generally not tax-deductible, unlike mortgage interest. The exception: if you use a personal loan specifically for business expenses and can document this, you may be able to deduct the interest as a business expense. Consult a tax professional for your specific situation.

Generally, no. Borrowing at 10–15% APR to invest in assets returning an uncertain 7–12% is a risky proposition — you could easily lose money on net. The exception is very high-confidence investments with returns clearly above your loan rate, though these carry inherent risk. Using borrowed money for investments also creates a dangerous dynamic: if the investment drops, you still owe the full loan. Build wealth from savings and earned income, not leverage.

Personal loans are a legitimate, powerful financial tool — when used strategically. With rates as low as 6.49% APR available to qualified borrowers in 2026, a personal loan can be dramatically cheaper than carrying high-interest credit card debt or financing purchases at retail rates. The key is knowing your credit score, understanding what you’ll actually pay in total, and shopping aggressively across multiple lenders before accepting any offer.

Your action checklist:

Once your loan is funded, build the financial foundation that keeps you from needing to borrow again. Use the 50/30/20 budget rule to allocate every dollar, build an emergency fund so unexpected expenses don’t become new debt, and protect your credit score for better loan rates next time. See: What Is a Good Credit Score? and Debt Consolidation Complete Guide.

💳 Smart Borrowers Also Use Cash Back Cards

Once your loan is under control, a $0-annual-fee cash back card earns you $300–$600/year on spending you’re already doing. See our top picks for 2026.

Be the first to leave a comment!

Leave a Comment