Use Spendzila's free calculators to apply what you learn in this article instantly.

Open Free Tools →It happens to almost everyone at some point — you forget a payment, your autopay fails, or you simply don’t have enough funds. Missing a credit card payment feels scary, but knowing exactly what happens next — and acting fast — can minimize the damage significantly.

In this guide, we’ll walk you through exactly what happens when you miss a credit card payment, how serious it really is depending on how long you wait, and the 5 steps you need to take right now to fix it.

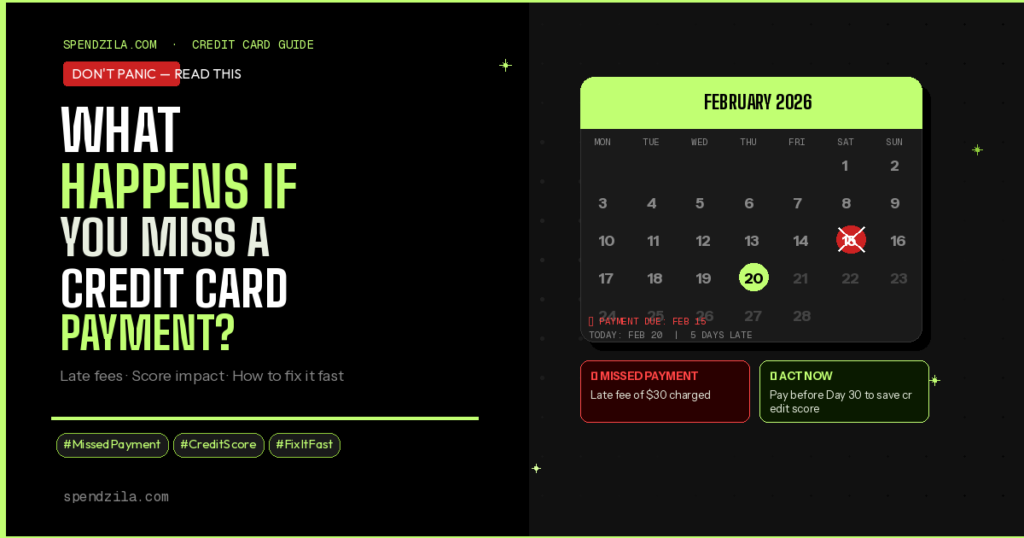

If you missed a payment less than 30 days ago — you’re in luck. You’ll pay a late fee but your credit score won’t be hurt yet. Call your issuer, pay now, and you may escape without any damage. Read on for the full breakdown.

The moment your payment due date passes without a payment, a series of events is set in motion. Here’s what happens in the first few hours and days:

The consequences of a missed payment get progressively worse the longer you wait. Here’s exactly what happens at each stage:

| Timeline | What Happens | Severity |

|---|---|---|

| Day 1–29 | Late fee charged ($30–$41). No credit score impact yet. Issuer sends reminders. | ⚠️ Minor |

| Day 30 | Reported to all 3 credit bureaus as 30-days late. Credit score drops 50–100+ points. | 🔶 Serious |

| Day 60 | Second late mark on credit report. Penalty APR may kick in (up to 29.99%). Score drops further. | 🔴 Severe |

| Day 90–120 | Account may be charged off. Debt sold to collections. Score tanks to 500s range. | 🚨 Critical |

| Day 180+ | Full charge-off. Collections calls begin. Legal action possible. Stays on credit report 7 years. | 💀 Devastating |

Payment history makes up 35% of your FICO score — it’s the single biggest factor. A missed payment is taken very seriously by the credit scoring system. Here’s what you can realistically expect:

| Current Score | Estimated Drop (30-Day Late) | New Approximate Score |

|---|---|---|

| 780 (Excellent) | –90 to –110 points | 670–690 (Good) |

| 720 (Good) | –60 to –80 points | 640–660 (Fair) |

| 660 (Fair) | –40 to –60 points | 600–620 (Poor) |

| 580 (Poor) | –20 to –40 points | 540–560 (Poor) |

Key insight: The higher your score, the more you have to lose. Someone with a 780 score loses far more points than someone with a 580 score — because the system penalizes unexpected negative behavior more harshly.

A late payment remains on your credit report for 7 years from the date of the missed payment. However, its impact on your score diminishes significantly over time. After 2 years of consistent on-time payments, most people see their score largely recover even with an old late payment still on file.

Whether you just missed a payment today or it’s been a few weeks, here’s exactly what to do:

Don’t wait. Log in to your account and pay at least the minimum amount due right this second. Every day you wait increases your risk of crossing the 30-day threshold where it gets reported to credit bureaus. Even a partial payment is better than no payment.

After paying, call the customer service number on the back of your card and politely ask for a late fee waiver. This works more often than people think — especially for first-time offenders with a good payment history. Use this script:

Check your credit report at AnnualCreditReport.com or use Credit Karma to see if the late payment has been reported. If it hasn’t (you’re under 30 days), you’ve dodged the bullet — focus on making sure it never happens again.

If the late payment has already been reported to the credit bureaus, you can write a formal goodwill letter to your credit card issuer asking them to remove it. This is a formal request where you acknowledge the mistake, show your strong payment history, and ask for a one-time removal.

Goodwill letters are not guaranteed to work, but they succeed surprisingly often — especially from long-standing customers with otherwise clean records. Send it via certified mail to the address listed on your statement.

Set up autopay for at least the minimum payment due on every credit card you have. This is the single most effective way to ensure you never miss a payment again. You can always pay extra manually, but autopay acts as your safety net.

Calling your issuer to waive a late fee takes about 5 minutes and works surprisingly often. Here’s the full approach:

Which issuers are most likely to waive fees?

Prevention is far better than recovery. Here’s a bulletproof system to ensure you never miss another payment:

Go to every single credit card account right now and enable autopay for the minimum payment due. You can always pay more manually, but this ensures you’re never reported late. Takes 2 minutes per card.

Call each card issuer and ask them to change your due date to the same day each month — ideally 5 days after your paycheck date. This makes it easy to remember and ensures funds are available. Most issuers allow this for free.

Add recurring calendar reminders 5 days before each payment due date. This gives you time to transfer funds if needed and double-check your autopay went through correctly.

Apps like Mint, YNAB (You Need a Budget), or Copilot show all your card balances and due dates in one place. A quick weekly check takes 60 seconds and keeps everything visible.

Always maintain a $200–$500 buffer in the account linked to your autopay. This prevents a missed payment caused by insufficient funds — one of the most common reasons autopay fails.

Not permanently, but it can cause serious short-term damage. A single 30-day late payment can drop your score by 50–110 points and stays on your report for 7 years. However, consistent on-time payments after the miss will steadily rebuild your score — most people recover significantly within 12–24 months.

Contact your issuer immediately and explain your situation. Many issuers have hardship programs that temporarily reduce or waive interest, lower minimum payments, or pause payments. These programs are rarely advertised but widely available — you just have to ask. Acting proactively is always better than ignoring the bill.

A late payment on one card is only reported on that specific account. However, some issuers have universal default clauses that allow them to raise your interest rate on their card if you miss a payment with a different lender. Check your cardholder agreements.

With consistent on-time payments afterward, most people see meaningful recovery within 12–24 months. The late payment remains on your report for 7 years but its scoring weight diminishes each year, especially as your positive payment history grows.

You can dispute it if it was reported in error — for example, if you paid on time but the payment wasn’t processed correctly. File a dispute with the credit bureau (Experian, Equifax, or TransUnion) and include proof of payment. If the late payment is accurate, disputing it won’t work — instead, try a goodwill letter to the issuer.

Yes. Credit card issuers can only report a payment as late to the credit bureaus once it is at least 30 days past due. A payment that is 1–29 days late results in a late fee but does not affect your credit score — as long as you pay before the 30-day mark.

Missing a credit card payment is stressful, but it’s not the end of the world — especially if you act fast. Here’s what to remember:

The single best thing you can do right now is set up autopay on every card you own. It takes 10 minutes and permanently eliminates your risk of missing a payment due to forgetfulness.

New to Credit Cards? Start Here

Learn how to choose, apply for, and use your first credit card the smart way.

Be the first to leave a comment!

Leave a Comment