Use Spendzila's free calculators to apply what you learn in this article instantly.

Open Free Tools →

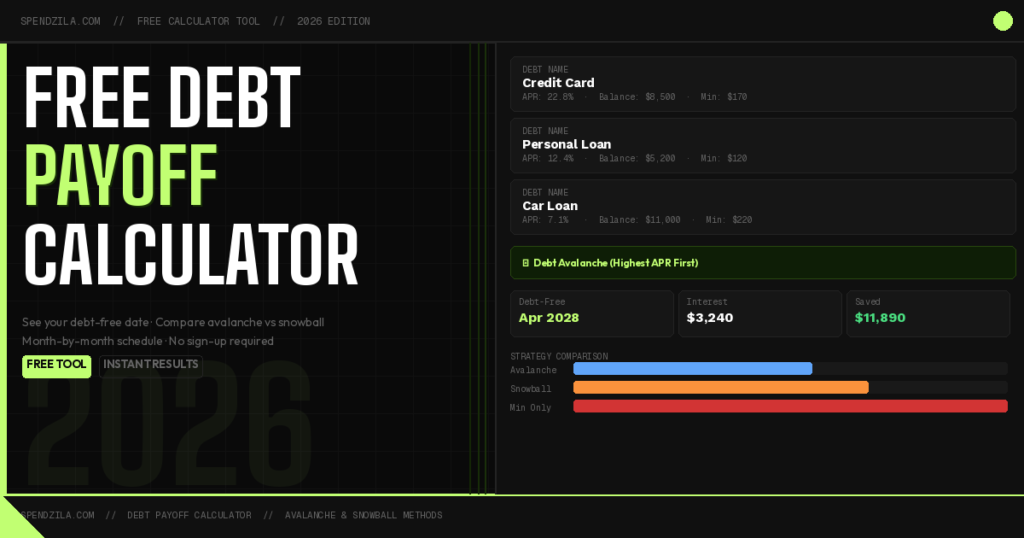

The Spendzila Debt Payoff Calculator shows your exact debt-free date, total interest cost, and a full month-by-month payment schedule — comparing the avalanche and snowball methods side by side. Enter your debts below and see your numbers in real time. No email required, no sign-up, completely free.

The calculator above works in four steps — and updates instantly as you type, so you can experiment with different scenarios in real time.

| Step | What to Enter | Where to Find It |

|---|---|---|

| 1. Debt Name | Label each debt (e.g. “Chase Visa”, “Car Loan”) | Your card or loan name |

| 2. Balance | Current amount owed on each debt | Your latest statement or app |

| 3. APR | Annual interest rate (e.g. 22.8 for 22.8%) | Back of your card or loan documents |

| 4. Min. Payment | Required minimum monthly payment | Your monthly statement |

| 5. Extra Payment | Any amount above minimums you can pay monthly | Your monthly budget surplus |

After entering your debts, toggle between Avalanche, Snowball, and Minimum Payments Only to instantly compare how much time and money each strategy saves. The month-by-month schedule shows exactly which debt gets paid first and when each account reaches $0.

The debt avalanche is the mathematically optimal debt payoff strategy. Here is the exact process:

Step 1: List all your debts from highest APR to lowest APR. Step 2: Pay the minimum on every debt. Step 3: Apply every extra dollar to the debt at the top of the list — the highest APR debt. Step 4: When that debt hits $0, take its entire payment (minimum + extra) and redirect it to the next-highest APR debt. Repeat until debt-free.

Because interest compounds daily on most credit cards, attacking the highest APR first minimizes how much interest accrues across the entire debt load. On a $25,000 debt load with mixed APRs, the avalanche method typically saves $2,000–$6,000 in total interest versus minimum payments alone, and 12–24 months versus the snowball method. The Consumer Financial Protection Bureau recommends the avalanche for consumers focused on minimizing total cost.

The debt snowball prioritizes psychology over math. Research published by Harvard Business Review found that the snowball method produces higher debt-free completion rates than the avalanche for most people — because eliminating an entire debt account creates a powerful motivational reward that sustains effort over a 2–3 year payoff journey.

The process: List all your debts from smallest balance to largest balance, regardless of APR. Pay minimums on all debts. Direct every extra dollar to the smallest balance. When it hits $0, add its entire payment to the next-smallest balance. Repeat. The growing “snowball” of freed-up payments accelerates with each elimination.

| Factor | Debt Avalanche | Debt Snowball |

|---|---|---|

| Target order | Highest APR → Lowest APR | Smallest balance → Largest balance |

| Total interest paid | Lower — mathematically optimal | Slightly higher |

| Time to first payoff | Depends on APR concentration | Faster — smallest balance first |

| Psychological reward | Delayed (months to first payoff) | Faster wins, higher motivation |

| Completion rate | High (for analytical people) | Higher (for most people) |

| Money savings | $1,000–$5,000+ more saved | Less savings, more wins |

| Best for | Data-driven, patient, high-APR spread | Motivation-driven, similar APRs |

Which should you choose? If your debts have a wide APR spread (e.g. a 26% credit card alongside a 7% car loan), the avalanche saves significantly more. If your debts have similar APRs, the difference is small and snowball’s psychological benefit wins. Use the calculator above to see the exact dollar and month difference for your specific debts.

The calculator shows your current trajectory. Here is how to change the numbers in your favor — ranked by impact:

1. Increase your extra monthly payment. Use the calculator’s extra payment slider to see how even $50–$100/month extra changes your debt-free date. On a $15,000 debt load, an extra $100/month often cuts 12–18 months off your timeline. Find this money by canceling subscriptions, meal prepping, or picking up one side shift per week.

2. Apply a 0% balance transfer card. Transferring your highest-APR credit card balance to a 0% APR card (available for 15–21 months for borrowers with 670+ credit scores) eliminates interest entirely during the transfer period. Enter the transferred balance at 0% APR in the calculator to see the exact savings. Use the NerdWallet balance transfer comparison to find current offers.

3. Call and negotiate lower APRs. A 2023 LendingTree survey found 69% of people who called and asked for a lower APR received one, averaging 4–6 percentage points lower. Try entering your current APR minus 5% in the calculator — see how much that one phone call is worth in dollars and months.

4. Apply windfalls 100% to your target debt. The average IRS tax refund was $3,011 in 2025. Applying that lump sum directly to your highest-APR debt has the same effect as paying an extra $250/month for an entire year. Enter a one-time lump sum in the calculator by reducing your target debt’s balance.

5. Add side income and automate the payment. Set up a separate bank account that receives your side hustle income (DoorDash, freelancing, selling unused items). Automate a transfer from that account to your target debt on the first of each month. The automation removes the decision — and decisions are where willpower fails. Check our complete debt elimination guide for the full 8-step system.

The calculator uses standard amortization math: monthly interest = (APR ÷ 12) × remaining balance. This matches the method used by banks and credit card issuers. The result is accurate to within 1–2 months for most debt scenarios. Minor variations can occur if your minimum payment is calculated as a percentage of your balance (which decreases over time) rather than a fixed amount.

For credit card debt at 22.8% APR, pay off the debt first — no investment reliably returns 22.8% annually. The exception: always contribute enough to your 401(k) to capture your employer match before making extra debt payments. The match is an immediate 50–100% return. For debt below 8% APR (mortgages, federal student loans), consider investing alongside debt repayment. See the CFPB debt repayment guidance for more detail.

The fastest path for $20,000 in mixed debt: (1) Transfer any credit card debt above 15% APR to a 0% balance transfer card. (2) Apply the debt avalanche to remaining debts. (3) Add $400–$600/month in extra payments via side income or expense cuts. (4) Apply any windfalls — tax refunds, bonuses — 100% to the target debt. This combination typically clears $20,000 in 28–40 months. Enter your specific numbers into the calculator above to get your exact timeline.

Yes — significantly. The second-largest factor in your FICO credit score is credit utilization (30% of your score). Paying down credit card balances directly reduces your utilization ratio, typically producing a 20–60 point score increase within 1–2 billing cycles of significant payoff. Eliminating a card entirely (while keeping it open) produces the largest utilization improvement.

Generally, no. Closing a paid card reduces your total available credit limit, which increases your credit utilization ratio and can lower your score. Keep paid cards open with a $0 balance (or one small recurring charge paid in full each month to keep them active). The exception: if the card charges an annual fee you will not recoup in rewards, closing may be worth the short-term score trade-off.

🎯 Know Your Numbers → Build Your Plan

Related: Pay Off Credit Card Debt · How to Get Out of Debt · Snowball vs Avalanche · Best Budgeting Apps 2026 · Build an Emergency Fund · How to Invest Money