Use Spendzila's free calculators to apply what you learn in this article instantly.

Open Free Tools →

| Scenario | Balance | Monthly Payment | Time to Pay Off | Total Interest |

|---|---|---|---|---|

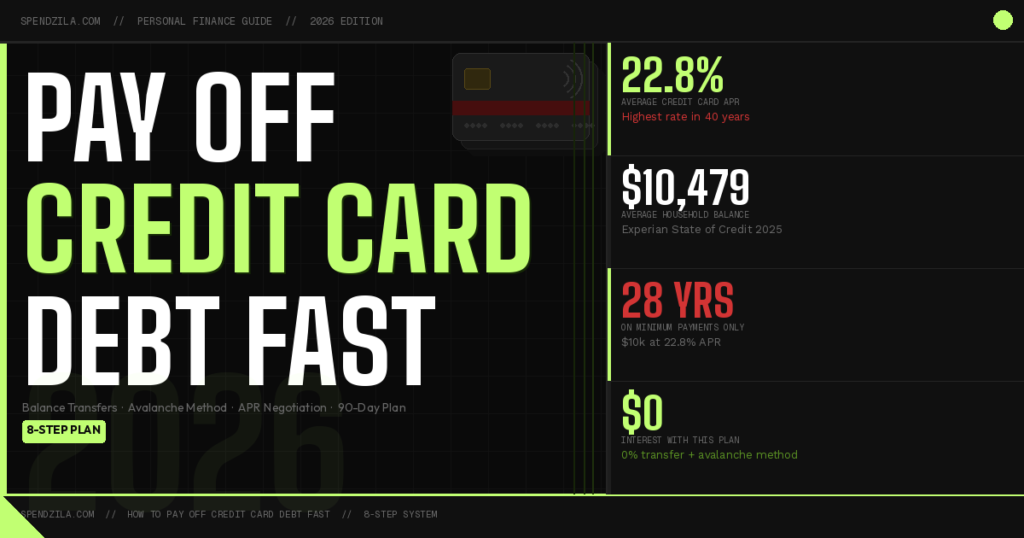

| Minimum payments only (~2%) | $10,000 | ~$200 | 28 years | $14,423 |

| $300/month fixed payment | $10,000 | $300 | 4 years 1 month | $4,792 |

| $500/month fixed payment | $10,000 | $500 | 2 years 2 months | $2,680 |

| $500/month + 0% balance transfer | $10,000 | $500 | 20 months | $0 |

Americans carry a collective $1.17 trillion in credit card debt as of Q4 2025, according to the Federal Reserve Bank of New York. The average household balance sits at $10,479 — costing $199 every single month in interest that buys absolutely nothing. Knowing how to pay off credit card debt is one of the highest-ROI financial skills you can develop. This 8-step plan works at every income level and has helped millions of Americans become credit-card-debt-free within 12–36 months.

The 2026 credit card crisis is not primarily about large balances — it is about interest rates. The average APR has hit 22.8% (Federal Reserve G.19, Q1 2026) — the highest in four decades. At that rate, $10,000 in credit card debt compounds $2,280 in annual interest. If your minimum payment this month is $200, roughly $190 of it disappears as interest, reducing your principal by just $10.

This is by design. The minimum payment formula — typically 1–2% of the balance — is calculated to keep you paying for decades. The fastest way to escape is to treat this as a math problem with a math solution: eliminate the interest rate (balance transfer), maximize your monthly payment (budgeting and side income), and target the highest-cost debt first (avalanche method). Each step below addresses one piece of that system.

You cannot build a payoff plan around numbers you don’t fully know. Most people who complete this step discover their total is 15–25% higher than their mental estimate. Pull every card statement — physical or digital — and fill in this table for each card you carry:

| Card / Issuer | Current Balance | APR | Minimum Payment | Monthly Interest Cost | Payoff Priority |

|---|---|---|---|---|---|

| Chase Sapphire | $___ | ___% | $___ | $___ | 🎯 Target if highest APR |

| Capital One Venture | $___ | ___% | $___ | $___ | — |

| Citi Double Cash | $___ | ___% | $___ | $___ | — |

| Store Card / Other | $___ | ___% | $___ | $___ | — |

| TOTAL | $___ | — | $___/mo | $___/mo | — |

The monthly interest cost column is the most motivating number in your entire financial picture. When you see “$220/month” evaporating as pure interest — buying nothing, reducing no balance, just gone — it creates urgency that no motivational content can match. Calculate it as: (Balance × APR) ÷ 12.

You cannot pay off a fire while adding fuel. If you are paying $400/month toward a card and charging $200/month in new purchases, your real progress is $200/month — not $400. Every new charge directly cancels your payment progress. The moment you commit to paying off credit card debt, the following must happen on the same day:

Delete all saved card information from Amazon, Apple Pay, PayPal, Google Pay, and every retail app and website. Research shows removing one-click purchasing reduces impulse spending by 40–60%. Remove your cards from your wallet — carry only your debit card. Switch recurring subscriptions on autopay to debit so cards have zero ongoing charges. If you need maximum friction, freeze your cards in a block of water. The time required for them to thaw is enough friction to eliminate most impulse purchases entirely.

Without a cash buffer, the cycle of credit card payoff is predictable and demoralizing: you pay $800 toward your card, a $600 car repair hits, and it goes right back on the card. You are back to zero — and motivation collapses with it. A $1,000 emergency buffer breaks this cycle permanently.

Financial planning research shows $1,000 covers 78% of all common financial emergencies — flat tires, medical copays, minor home repairs, vet bills. Build this before making any extra debt payments. Keep it in a high-yield savings account earning 4–5% APY, separate from your checking account, accessible within one business day but not linked to daily spending. Most people accumulate $1,000 within 30–60 days through subscription cancellations and selling unused items.

A 0% APR balance transfer card allows you to move existing high-interest credit card debt to a new card that charges zero interest for 15–21 months. During this window, every dollar you pay reduces your principal — not interest. As shown in the table above, $500/month with a 0% balance transfer eliminates $10,000 in 20 months with $0 in interest paid. Without it, the same payment at 22.8% APR takes 26 months and costs $2,680 in interest charges.

| Card | 0% APR Period | Transfer Fee | Credit Score Needed | Best For |

|---|---|---|---|---|

| Citi Simplicity® Card | 21 months | 3% (min $5) | 670+ | Longest 0% window available |

| Wells Fargo Reflect® Card | 21 months | 5% (min $5) | 670+ | Large balance transfers |

| Chase Slate Edge℠ | 18 months | 3% (min $5) | 670+ | Lower transfer fee |

| Discover it® Balance Transfer | 18 months | 3% (min $5) | 670+ | Cashback on new purchases |

Balance transfer math: A 3% fee on $10,000 = $300. At 22.8% APR you were paying $2,280/year in interest. The transfer fee pays for itself in under 7 weeks. Three rules you must follow: (1) Do not use the new card for purchases — new purchases on balance transfer cards often accrue interest immediately. (2) Pay the full transferred balance before the 0% period ends — the go-to APR after promotion is typically 20–29%. (3) Keep your old cards open at $0 balance to protect your credit utilization ratio.

If your credit score is below 670, skip this step for now. Focus on Steps 5–8, make 6–12 months of consistent on-time payments, and reapply once your score improves. Monitor your score for free via Credit Karma or Experian.

Once you know your balances and APRs, you need a clear targeting system. There are two proven methods — and the right one depends on how you are wired, not which one looks better on paper.

Pay the minimum on every card. Apply every extra dollar to the card with the highest APR. When that card is cleared, redirect its entire payment to the next-highest APR card. Repeat until all cards are eliminated. This method is mathematically optimal — it minimizes total interest paid and typically saves $1,000–$5,000 more than the snowball on a $20,000+ debt load. Best for: analytical, patient people who are motivated by data and numbers over quick wins.

Pay the minimum on every card. Apply every extra dollar to the card with the smallest balance. When that card is eliminated, redirect its entire payment to the next-smallest balance. This creates faster psychological wins — eliminating an account entirely produces a motivating reward. Harvard Business Review research found higher debt-free completion rates for snowball users. Best for: people who need visible wins to maintain motivation over a 1–3 year payoff journey.

| Factor | Choose Avalanche | Choose Snowball |

|---|---|---|

| Motivation style | Data-driven, patient | Needs wins to keep going |

| APR spread | Large gap between cards | Similar APRs across cards |

| Total interest savings | Higher — mathematically optimal | Slightly less |

| Completion rate | High (for analytical people) | Higher (for most people) |

Both methods work. The one you will actually execute consistently for 18–36 months is the correct choice. Pick one today — do not switch midway unless your debt profile changes significantly.

A zero-based budget assigns every dollar of your monthly take-home income to a specific category before the month begins — so that income minus all assignments = $0. This does not mean spending everything. It means every surplus dollar is intentionally assigned to debt payoff rather than drifting into discretionary spending.

The process: (1) Write your total monthly take-home income. (2) Subtract fixed necessities: rent, utilities, insurance, grocery budget, minimum payments on all cards. (3) Cut every non-essential category to the minimum during your debt-attack period. (4) Assign every remaining dollar to your target card’s extra payment. Use YNAB (You Need A Budget) for automatic tracking, or see our guide to the best free budgeting apps in 2026.

| Category | Priority During Payoff | Action |

|---|---|---|

| Rent / Mortgage | Non-negotiable | Pay first, always |

| Utilities + Internet | Non-negotiable | Call to negotiate lower rates |

| Groceries | Essential — reduce amount | Meal prep, store brands only |

| Minimum payments — all cards | Non-negotiable | Set to autopay — never miss |

| Streaming subscriptions | Cut to 1 maximum | Cancel all but one |

| Dining out / food delivery | Cut drastically | Cook at home, Sunday meal prep |

| Entertainment / shopping | Pause entirely | Temporary — not permanent |

| Extra payment — target card | 🎯 Every remaining dollar | Automate on payday |

The speed of your credit card payoff is directly proportional to how much extra you can apply to your target card each month. Every additional $100/month cuts 6–12 months off a $15,000 debt load at 22.8% APR. Here is where to find it, ranked by speed of impact:

Cut immediately — same day, 30–60 minutes of work: Cancel unused streaming subscriptions ($8–$22/month each), gym memberships you rarely use ($20–$60/month), unused app subscriptions, and subscription boxes. The average American pays for 4.5 subscriptions they barely use. One hour of cancellations typically recovers $80–$200/month permanently.

Reduce ongoing spending: Meal prep instead of ordering delivery — the average American spends $166/month on food delivery apps, which drops to near zero with Sunday meal prep ($120–$150/month saving). Switch to store-brand groceries — national brands carry a 25–40% premium over store equivalents with near-identical quality ($40–$100/month saving). Cut cable if you still have it ($80–$150/month saving). Switch to a cheaper cell phone plan ($30–$60/month saving).

Earn more: Sell unused items on Facebook Marketplace and eBay — a full home sweep typically generates $200–$800 in immediate lump-sum payments toward your target card. Delivery driving (DoorDash, Uber Eats, Instacart) pays $15–$22/hour after expenses — 10–15 hours per weekend generates $200–$350/month. Freelancing on Upwork or Fiverr can generate $300–$1,500/month within 2–3 months for anyone with a marketable skill (writing, design, coding, tutoring, accounting).

The windfall rule — the single highest-impact habit: Apply 100% of every unexpected dollar directly to your target card before spending any of it — tax refunds (average $3,011 in 2025 per the IRS), work bonuses, cash gifts, insurance settlements, and side hustle payouts. Windfall discipline alone cuts 6–18 months from most payoff timelines.

This step is dramatically underused and takes 10 minutes per card. A 2023 LendingTree survey found that 69% of cardholders who called and requested a lower APR received one, with an average reduction of 4–6 percentage points. On an $8,000 balance, a 5% APR reduction saves $400/year — for a single 10-minute call. Do this for every card, every year.

Call the number on the back of your card. Ask for account services or the retention department. Then say:

If they say yes: Confirm the new rate and effective date. Set a calendar reminder to call again in 12 months. If they say no: Ask to speak with the retention department specifically. Ask what your account would need to look like to qualify. Note the date and representative name, and call back in 6 months — approval criteria update quarterly.

If refused again: This is the moment to consider a balance transfer (Step 4) or nonprofit credit counseling, which negotiates rates on your behalf through formal agreements with issuers — often achieving 6–9% on cards currently at 22%+.

The same 8 steps apply at low income, but with adjusted priorities. When income is already tight, two principles take precedence over all others:

Apply for every assistance program you qualify for. Benefits.gov lists federal and state programs by location. SNAP food assistance, LIHEAP utility assistance, Medicaid health coverage, and local food banks can free up $200–$600/month that was previously going to food, utilities, and healthcare — money that can now directly attack credit card debt. Many people leave significant assistance unclaimed simply because they have not applied.

Focus on income increase before expense cuts. At $28,000/year, there is a floor below which expense cuts become harmful — to health, nutrition, and transportation. Adding $300–$500/month via delivery driving or freelance work is frequently more impactful than squeezing a budget that is already minimal.

Use nonprofit credit counseling. NFCC (National Foundation for Credit Counseling) member agencies offer free or sliding-scale debt management plans that negotiate directly with credit card companies — often achieving rates of 6–9% on cards currently charging 22–29%. For people overwhelmed by multiple high-APR cards, this frequently outperforms the DIY approach.

Bankruptcy as a genuine last resort. If your credit card debt exceeds two to three times your annual income with no realistic path to higher earnings, consult a bankruptcy attorney — many offer free initial consultations. Chapter 7 bankruptcy discharges most unsecured debt within 3–6 months. It is a legal tool designed for financial hardship, not a failure. The U.S. Courts bankruptcy page explains the process in plain language.

WEEK 2 — BUILD YOUR SYSTEM

☐ Complete your zero-based budget (YNAB free trial or spreadsheet)

☐ Choose your strategy: avalanche (highest APR) or snowball (smallest balance)

☐ Set autopay minimums on ALL cards — never miss a minimum payment

☐ If credit score 670+: apply for a 0% APR balance transfer card

☐ Call each card issuer — use the negotiation script from Step 8

MONTH 2 — ATTACK

☐ $1,000 emergency buffer complete — keep separate, don’t touch it

☐ Complete balance transfer to 0% card (if approved)

☐ Sell $200–$500 of unused items — apply 100% to target card

☐ First extra payment hits target card — screenshot the new balance

☐ Research one side income option: delivery driving, freelancing, Fiverr

MONTH 3 — BUILD MOMENTUM

☐ Calculate months saved by your extra payments — write it down

☐ Launch one side income stream — first payout goes 100% to debt

☐ Apply any tax refund received directly to target card

☐ Calculate your debt-free date — write it somewhere you see it every day

Paying off credit card debt is ultimately about deciding that future financial freedom is worth present sacrifice. The people who become credit-card-debt-free are not people with higher incomes — they are people who built a system and executed it consistently for 18–36 months. Use this 8-step plan, adapt it to your situation, and commit to your debt-free date.

🎯 Credit Cards Done → Eliminate All Debt

Related: How to Get Out of Debt · Snowball vs Avalanche Guide · How to Save Money Fast · Best Budgeting Apps 2026 · Build an Emergency Fund · How to Invest Money