Use Spendzila's free calculators to apply what you learn in this article instantly.

Open Free Tools →Takes under 2 minutes. Full step-by-step guide with examples below.

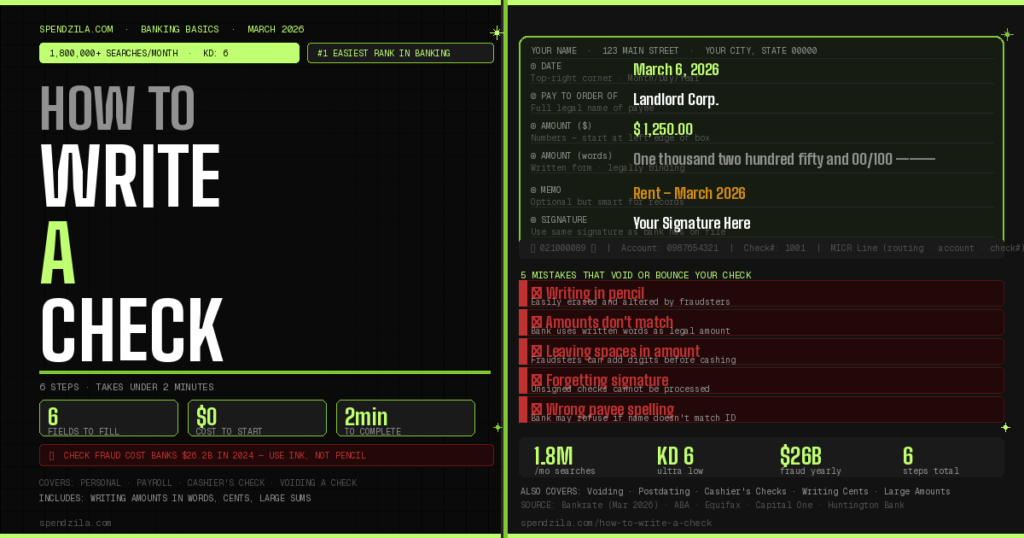

Writing a check may seem old-fashioned in 2026 — but millions of Americans still write them every day for rent, contractor payments, government fees, gifts, and situations where digital payments aren’t accepted. If you’ve never written one before, or it’s been a while, this complete guide walks you through every field on the check, shows you exactly what to write, and covers every common variation — cents, large amounts, voiding, endorsing, and more.

Before writing your first check, it helps to understand what each part of the check does. Here is every field labeled:

| Field | Location on Check | What It Is | Required? |

|---|---|---|---|

| Your name & address | Top-left | Pre-printed. Your information for the payee and bank. | Pre-printed |

| Check number | Top-right | Sequential number for your records (e.g., 1042) | Pre-printed |

| ① Date | Top-right corner | When the check was written | Required |

| ② Pay to the order of | Below date, long line | Name of the person or company you’re paying | Required |

| ③ Amount box ($) | Right side, small box | Payment amount in numbers (e.g., $1,250.00) | Required |

| ④ Written amount | Long line below payee | Payment amount in words — legally binding if different from box | Required |

| ⑤ Memo line | Bottom-left | What the check is for — your notes | Optional |

| ⑥ Signature | Bottom-right | Authorizes bank to release funds — check is invalid without it | Required |

| Routing number | Bottom-left MICR line | 9-digit number identifying your bank | Pre-printed |

| Account number | Bottom-center MICR line | Your unique bank account number | Pre-printed |

Let’s walk through every step of writing a check for a real example: paying $1,250.00 rent to your landlord “Lakeview Properties LLC” on March 6, 2026.

Where: Top-right corner, on the line labeled “Date”

What to write: Today’s date — month, day, and year

You can write it in any of these accepted formats:

Important notes: An undated check can technically be cashed at any time, creating recordkeeping chaos. Always date it. Some people “postdate” a check by writing a future date — but most banks will process checks immediately regardless of the date written. Never backdate a check — that can constitute fraud.

Where: The long line after “Pay to the order of”

What to write: The full legal name of the person or company you’re paying

For our example: Lakeview Properties LLC

Tips: Use the payee’s exact legal name — not a nickname. For a business, use the exact registered name. If paying a person, write their first and last name as it appears on their ID. Misspelling a name can cause delays or refusal to cash. You can write “Cash” instead of a name, but this is risky — if the check is lost or stolen, anyone can cash it.

Where: The small box on the right side, to the right of the “$” symbol

What to write: The payment amount in numbers, starting as far left as possible

For our example: 1,250.00

Anti-fraud tip: Always start writing the number at the very left edge of the box. This leaves no space for anyone to add digits before it. After writing the amount, draw a horizontal line through any remaining blank space in the box. Never write “1,250” — always include the cents as “.00” even when paying a round number.

Where: The long line below the “Pay to the order of” line, to the left of “dollars”

What to write: The full dollar amount spelled out in words, then the cents as a fraction

For our example: One thousand two hundred fifty and 00/100 ———————

Where: Bottom-left, on the line labeled “Memo” or “For”

What to write: A brief note about the payment’s purpose

For our example: Rent – March 2026

The memo line is optional but highly recommended. It creates a paper trail for your records, helps the payee apply the payment correctly, and is sometimes required by the payee (e.g., a business may ask you to write your account number or invoice number). It has no legal significance — it does not change who gets paid or how much.

Where: The line in the bottom-right corner

What to write: Your signature — exactly as your bank has it on file

Your signature is what legally authorizes your bank to release funds from your account to the payee. A check without a signature cannot be cashed or deposited. Use the same signature consistently — mismatched signatures can trigger fraud alerts or processing delays. Sign only after all other fields are completed. Never sign a blank check.

The written word line trips up most first-time check writers. Here is the exact formula followed by examples for every common amount:

The Formula: [Dollar amount in words] and [cents]/100 ————

| Number Amount | Written Amount (what to write on the line) |

|---|---|

| $10.00 | Ten and 00/100 ———————————————— |

| $25.50 | Twenty-five and 50/100 ——————————— |

| $47.65 | Forty-seven and 65/100 ——————————— |

| $100.00 | One hundred and 00/100 —————————— |

| $500.00 | Five hundred and 00/100 —————————— |

| $750.50 | Seven hundred fifty and 50/100 ———————— |

| $1,000.00 | One thousand and 00/100 —————————— |

| $1,250.00 | One thousand two hundred fifty and 00/100 ——— |

| $1,500.00 | One thousand five hundred and 00/100 ———— |

| $2,000.00 | Two thousand and 00/100 —————————— |

| $5,000.00 | Five thousand and 00/100 —————————— |

| $10,000.00 | Ten thousand and 00/100 —————————— |

Writing cents is the step that confuses most people. The rule is simple: write the cents as a fraction out of 100, directly after the word “and”.

Example — $236.79:

Example — $12.05:

For round dollar amounts (no cents):

| Amount | Number Box | Written Line |

|---|---|---|

| $1,000 | 1,000.00 | One thousand and 00/100 —— |

| $1,500 | 1,500.00 | One thousand five hundred and 00/100 —— |

| $2,000 | 2,000.00 | Two thousand and 00/100 —— |

| $5,000 | 5,000.00 | Five thousand and 00/100 —— |

| $10,000 | 10,000.00 | Ten thousand and 00/100 —— |

| $25,000 | 25,000.00 | Twenty-five thousand and 00/100 —— |

You may need to void a check in two situations: (1) you made a mistake while writing it, or (2) someone asks for a “voided check” to set up direct deposit or automatic payments.

Employers and payment services often ask for a voided check to set up direct deposit or automatic ACH payments. They need your routing and account numbers from the MICR line at the bottom. Simply:

Alternative: Most banks allow you to print an official direct deposit form or provide a pre-filled form from your online banking portal — this is safer than handing over a physical voided check. Ask your bank if you prefer this option.

When you receive a check and want to cash or deposit it, you must endorse it by signing the back. There are three types of endorsements:

| Endorsement Type | What to Write | Use Case |

|---|---|---|

| Blank endorsement | Just your signature | Cashing at your bank in person — most common |

| Restrictive endorsement | “For deposit only” + your signature | Mobile deposit or mailing a check — limits fraud if lost |

| Special endorsement | “Pay to the order of [Name]” + your signature | Signing the check over to a third party |

For mobile deposit: Many banks in 2026 require you to write “For mobile deposit only at [Bank Name]” under your signature. Check your bank’s mobile app for their specific endorsement requirement before scanning.

| Check Type | What It Is | When to Use | Cost |

|---|---|---|---|

| Personal check | Drawn on your personal checking account | Everyday payments — rent, gifts, contractors | Free (part of account) |

| Cashier’s check | Issued and guaranteed by the bank itself | Large purchases (cars, real estate down payment) | $5–$15 fee |

| Certified check | Personal check verified and guaranteed by your bank | When payee requires guaranteed funds | $10–$20 fee |

| Money order | Prepaid, issued by bank or USPS | No checking account, or when personal checks not accepted | $1–$5 fee |

| Payroll check | Issued by an employer for wages | Receiving your paycheck | Free to receive |

| Mistake | What Goes Wrong | The Fix |

|---|---|---|

| Writing in pencil | Easily erased and altered by fraudsters | Always use blue or black ink pen — black gel ink is best |

| Numbers don’t match words | Bank uses the written word amount — could overpay or underpay | Double-check both fields before signing |

| Leaving spaces in amounts | Fraudsters can insert digits, multiplying the amount | Start at left edge of box; draw a line after written amount |

| Forgetting to sign | Check is invalid — cannot be cashed or deposited | Make signing the final step every time |

| Signing a blank check | Anyone who finds it can fill in any amount and cash it | Always complete all fields before signing |

Check fraud cost US financial institutions $26.2 billion in 2024 and is growing rapidly due to “check washing” — a scam where criminals intercept checks in the mail, chemically remove the ink, and rewrite them for larger amounts to different payees. Here is how to protect yourself:

Writing your first check takes under 2 minutes once you know what goes where. Fill in: (1) today’s date top-right, (2) the payee’s full name, (3) the dollar amount in numbers in the small box, (4) the dollar amount in words on the long line, (5) a memo note if needed, and (6) your signature bottom-right. Use a pen, not a pencil, and double-check that both amounts match before signing.

Write the cents as a fraction after the word “and”. For $47.65: number box = 47.65; written line = Forty-seven and 65/100. For round amounts, write “00/100” — e.g., Five hundred and 00/100.

Number box: 1,000.00. Written line: One thousand and 00/100 ————. Always draw a line after the written amount to fill remaining blank space.

Void it and start fresh. Write “VOID” in large capital letters across the entire check face. Never try to cross out and correct a mistake on a check — banks may refuse to process it, and it looks suspicious. Keep the voided check as a record, or shred it immediately.

Yes — write your own name on the “Pay to the order of” line. This is a legitimate way to move money between your accounts or withdraw cash. Endorse the back normally when depositing.

Writing a future date on a check in hopes the recipient will wait to cash it. However, most US banks will process a postdated check immediately regardless of the date written. Do not rely on postdating to delay payment — use your bank’s scheduled bill pay feature instead.

Sign your name on the back endorsement line, then write “For mobile deposit only” (or your bank may require “For mobile deposit only at [Bank Name]”) below your signature. Check your bank’s app for their exact requirement — some banks reject mobile deposits without this restriction.

The routing number is the 9-digit number in the bottom-left of the check, marked by the ⑆ symbol on each side. It identifies your specific bank. Your account number follows it on the same line. You’ll need both for setting up direct deposit and automatic payments.

For legitimate direct deposit or ACH setup purposes, yes — a voided check from a trusted employer or financial institution is safe. However, your routing and account numbers are still visible on a voided check, so only provide voided checks to trusted parties. As an alternative, most banks let you print a direct deposit authorization form from online banking that serves the same purpose.

Personal checks are generally valid for 180 days (6 months) from the date written, according to UCC Section 4-404. After that, banks may legally refuse to process them as “stale checks.” Government and payroll checks may have different expiration rules — always check the front of the check for any “void after” date printed by the issuer. If you have a check older than 6 months, contact the issuer for a replacement.

🏠 Ready to Open Your First Checking Account?

Now that you know how to write a check, make sure your money is working for you. The best checking accounts in 2026 offer zero fees, high-yield interest, and instant mobile deposits.

Related Spendzila Guides:

→ How to Save Money Fast in 2026

→ 50/30/20 Budget Rule — The Complete Guide

→ Best Personal Loans 2026 — Rates from 6.99%

→ Current Average Credit Score in the US 2026

→ How to Improve Your Credit Score — 11 Steps

Manage your cookie preferences below. Essential cookies are required for the site to work. Your financial calculator data is never stored in cookies.

Necessary for basic site functionality — navigation and forms. Cannot be disabled.

Google Analytics (anonymized) — helps us understand how visitors use the site. No personal data collected.

Google AdSense — used to show relevant ads. Helps keep Spendzila free for everyone.

Remember your last-used tool or tab for a better experience. No financial data stored.

Be the first to leave a comment!

Leave a Comment