📥 Monthly Income

📊 Budget Summary

Use Spendzila's free calculators to apply what you learn in this article instantly.

Open Free Tools →

| Category | Rule % | On $4,000/mo | On $6,000/mo | Examples |

|---|---|---|---|---|

| Needs | 50% | $2,000 | $3,000 | Rent, groceries, utilities, insurance, min. payments |

| Wants | 30% | $1,200 | $1,800 | Dining, streaming, shopping, gym, travel |

| Savings + Debt | 20% | $800 | $1,200 | Emergency fund, 401k, extra debt payments, investments |

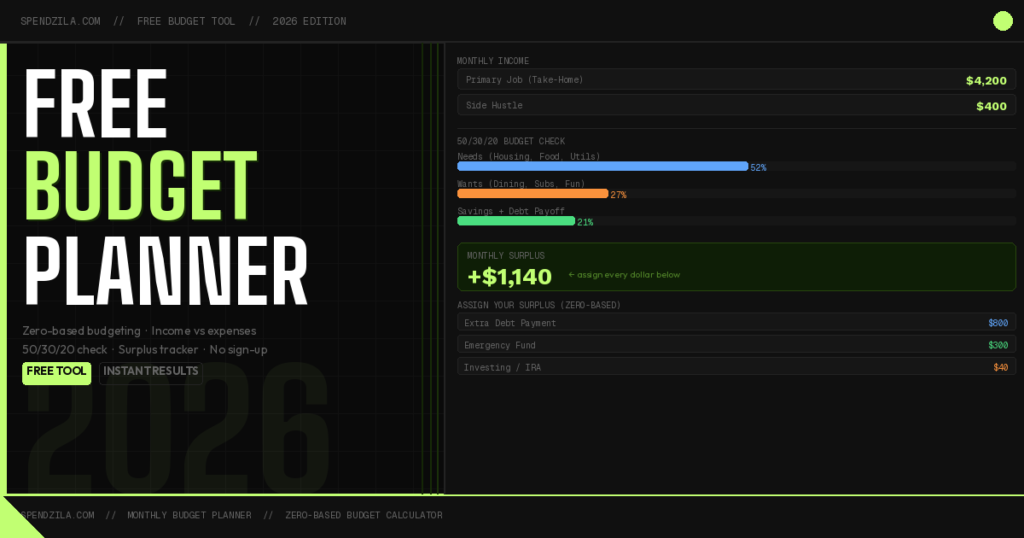

A budget planner is the single most important financial tool you can use — before investing, before paying off debt, before any financial goal. Without knowing exactly where your money goes each month, every other financial decision is made in the dark. The Spendzila Budget Planner below builds your complete zero-based monthly budget in under 5 minutes, calculates your surplus or deficit in real time, and shows exactly how much you can free up for debt payoff or savings.

The budget planner works in four sections — and every number updates in real time as you type. Use the pre-loaded templates (Tight Budget, Comfortable, Debt Attack Mode) to get started instantly, then adjust the numbers to match your actual situation.

| Section | What to Enter | Pro Tip |

|---|---|---|

| Income | All take-home income after taxes — salary, side hustle, freelance, rental | Use your actual bank deposits, not your gross salary |

| Fixed Expenses | Rent, car payment, insurance, phone, loan minimums — same every month | These are non-negotiable — focus cuts on variable expenses first |

| Variable Expenses | Groceries, dining, gas, entertainment — average your last 3 months | Check your bank statement — most people underestimate by 20–30% |

| Assign Surplus | Name a goal for every remaining dollar — debt payoff, emergency fund, investing | Zero-based means $0 unassigned — every dollar has a job |

Zero-based budgeting (ZBB) is the most effective personal budgeting method for people with financial goals — whether paying off debt, building an emergency fund, or saving for a house. The concept: your monthly income minus every assigned category equals $0. Not because you spend everything — but because every dollar, including savings and debt payments, is intentionally assigned a job before the month begins.

Traditional budgeting tracks spending after it happens. Zero-based budgeting assigns spending before it happens. This shift — from reactive to proactive — is why ZBB users consistently outperform traditional budgeting in debt payoff studies and savings rate benchmarks. The tool above automates the zero-based calculation: enter your income and expenses, then use the “Assign Surplus” section to give every remaining dollar a destination.

The 50/30/20 rule is the most widely cited budgeting framework, popularized by Senator Elizabeth Warren in her book All Your Worth. It divides after-tax income into three buckets:

50% — Needs: Housing, food, utilities, transportation, insurance, and minimum debt payments. These are expenses you cannot easily eliminate. If your needs exceed 50% of take-home income, the two levers are increasing income or finding a cheaper housing or transportation situation.

30% — Wants: Dining out, streaming services, gym memberships, clothing beyond basics, entertainment, travel, hobbies. During debt payoff, reducing this bucket to 10–15% is the fastest way to free up cash for extra debt payments without touching fixed necessities.

20% — Savings + Debt Payoff: Emergency fund contributions, retirement account contributions (at least enough for your employer 401k match), and extra debt payments beyond minimums. During aggressive debt payoff, this bucket can be expanded to 30–40% by cutting the wants bucket temporarily.

The Federal Reserve’s Report on the Economic Well-Being of U.S. Households found that 37% of Americans could not cover a $400 emergency without borrowing — a sign that savings allocations in the 20% bucket are frequently underfunded or nonexistent.

| Category | Recommended % of Take-Home | On $5,000/mo Take-Home | Warning Sign |

|---|---|---|---|

| Housing (rent/mortgage) | 25–35% | $1,250–$1,750 | Above 40% — financially vulnerable |

| Food (groceries + dining) | 10–15% | $500–$750 | Above 20% — dining likely too high |

| Transportation (car + gas) | 10–15% | $500–$750 | Above 20% — consider refinancing car loan |

| Subscriptions + Entertainment | 3–5% | $150–$250 | Above 8% — subscription creep |

| Debt Payments (min + extra) | 15–20% during payoff | $750–$1,000 | Below 10% — payoff will take decades |

| Emergency Fund / Savings | 10–20% | $500–$1,000 | $0 — any emergency goes on credit card |

| Retirement (401k / IRA) | At least employer match | $250–$500 minimum | $0 with employer match — leaving free money |

Once the budget planner reveals your deficit or your overspending categories, here is where to cut — ranked by ease of implementation and typical dollar impact:

Cancel unused subscriptions (same day, $50–$200/month). The average American pays for 4.5 subscriptions they barely use. Pull up your bank statement and cancel anything you haven’t actively used in the past 30 days — streaming services, gym memberships, app subscriptions, subscription boxes. According to CNBC research, the average household spends $219/month on subscriptions, often without realizing it. One hour of cancellations = $100–$200/month recovered permanently.

Cut food delivery to zero or near-zero ($100–$180/month). The average American spends $166/month on DoorDash, Uber Eats, and similar apps. Meal prepping on Sundays reduces this to near zero while improving nutrition. This single change frees up $120–$160/month with zero impact on nutrition or food enjoyment.

Switch to store-brand groceries ($40–$100/month). National brand groceries carry a 25–40% price premium over store equivalents with near-identical ingredients and quality. Switching fully to store brands on staples (pasta, canned goods, dairy, bread) saves $40–$100/month with no lifestyle impact.

Audit your insurance policies ($30–$80/month). Car and home/renters insurance premiums increase 8–15% per year at renewal without notification. Calling your insurer and shopping competitors every 12–18 months via Policygenius or similar comparison sites typically saves $30–$80/month.

Refinance high-rate debt ($50–$200/month). If you have a car loan above 9% APR or personal loans above 15% APR, refinancing through a credit union or online lender can reduce monthly payments significantly. Use the freed-up payment as extra debt payoff money. See our credit card debt guide and debt payoff calculator to model the impact.

The best budgeting method is the one you will consistently execute. For most people, zero-based budgeting produces the best financial outcomes because it requires active allocation of every dollar. The 50/30/20 rule is an excellent starting framework for people new to budgeting. The envelope method (cash-only for discretionary spending) works well for people who overspend using cards. Use the planner above to implement zero-based budgeting digitally — it handles all the math automatically.

Budget based on your lowest expected monthly income, not your average. Treat any income above that floor as a windfall — apply 50% to savings/debt and spend 50% freely. This approach, recommended by NFCC financial counselors, prevents the feast-or-famine spending pattern that keeps irregular earners financially unstable.

A starter $1,000 emergency fund can typically be built within 30–60 days through subscription cancellations and selling unused items. A full 3–6 month emergency fund ($8,000–$20,000 for most households) takes 12–36 months at a $500–$800/month savings rate. Keep your emergency fund in a high-yield savings account earning 4–5% APY — the interest compounds while it sits.

The budget comes first — always. A budget is how you find the extra money to accelerate debt payoff. Without a budget, you cannot identify where to cut or how much extra you can apply to debt each month. Build your budget using the planner above, identify your monthly surplus, then use our debt payoff calculator to apply that surplus to your highest-APR debt.

🎯 Budget Built → Now Attack the Debt

Related: Debt Payoff Calculator · Pay Off Credit Card Debt · Get Out of Debt · Build an Emergency Fund · How to Invest Money · Best Budgeting Apps 2026